Comments on “The Hyperglobalization of Trade and Its Future,” by Arvind Subramanian and Martin Kessler

Bernard Hoekman

A distinctive feature of the post–World War II period has been the rapid increase in international commerce, which, with the exception of a few episodes when the world went into recession (most notably in 2008), has grown more rapidly than output year in, year out. The extent to which world trade has grown since the 1950s is truly phenomenal, especially when put in historical perspective. The volume of trade increased 27-fold between 1950 and 2008, three times more than the growth in global GDP. The value of global trade in goods and services passed the $20 trillion mark in 2011 (WTO 2012), reaching 59 percent of global GDP, up from 39 percent in 1990.1

Subramanian and Kessler provide an interesting overview of several important dimensions of the most recent wave of globalization, which started in the early 1990s, including the increasing share of global output and trade by developing countries, especially China; the growing role of services; and the proliferation of preferential trade agreements (PTAs). They also highlight a number of important policy implications of recent trends, in particular the need for governments to address the adjustment costs of globalization and to mobilize the necessary funding for social expenditures and continued (greater) investment in education. In what follows, I provide a complementary view of some of the key challenges that confront policymakers, in particular increasing the participation in supply networks by the large number of countries that do not do so today and reducing the large current account imbalances that have emerged and that are putting pressure on the trading system.

Trade Costs Have Been Declining, but the World Is Not Close to Being Flat

The basic driver of the developments Subramanian and Kessler describe has been the steep fall in trade costs, as a result of technological change and the adoption of outward- (export-) oriented policies. Technological changes have been both hard and soft. They include advances in information and communication technology (ICT), which led to a sharp drop in the costs of international telecommunications, and the adoption of containerization and other improvements in logistics, which led to a sharp fall in unit transport costs. Average tariffs were in the 20–30 percent range in 1950 (WTO 2007), complemented by a plethora of nontariff barriers (including quantitative restrictions and exchange controls) that were often more binding. Today the average uniform tariff equivalent in OECD countries for merchandise trade is only 4 percent, mostly reflecting protection of agriculture, and the average level of import protection around the world has dropped to 5–10 percent (Kee, Nicita, and Olarreaga 2009).

Bernard Hoekman is a professor at and the director of the Global Economics Program at the Robert Schuman Centre for Advanced Studies at the European University Institute and a research fellow at the Centre for Economic Policy Research, in London. These comments were prepared for the Towards a Better Global Economy Project funded by the Global Citizen Foundation. The author alone is responsible for the content. Comments or questions should be directed to Bernard.Hoekman@EUI.eu.

1 Trade openness ratios were calculated from the World DataBank (the World Bank’s Global Economic Prospects database).

This increase in internationalization as a result of the fall in trade costs reflects ever greater “vertical specialization,” with firms (plants) in different countries concentrating on (specializing in) different parts of the value chain for a final product. As a result, the share of manufactures in total exports of developing countries has increased from just 30 percent in 1980 to more than 70 percent today, with a substantial proportion of this increase made up of intraindustry trade—the exchange of similar, differentiated products. Since the 1990s, intraindustry trade ratios for high-growth developing countries and transition economies have risen to 50 percent or higher. Much of this trade is intraregional—for example, about half of all East Asian exports of manufactures go to other East Asian economies, often as part of a supply chain.

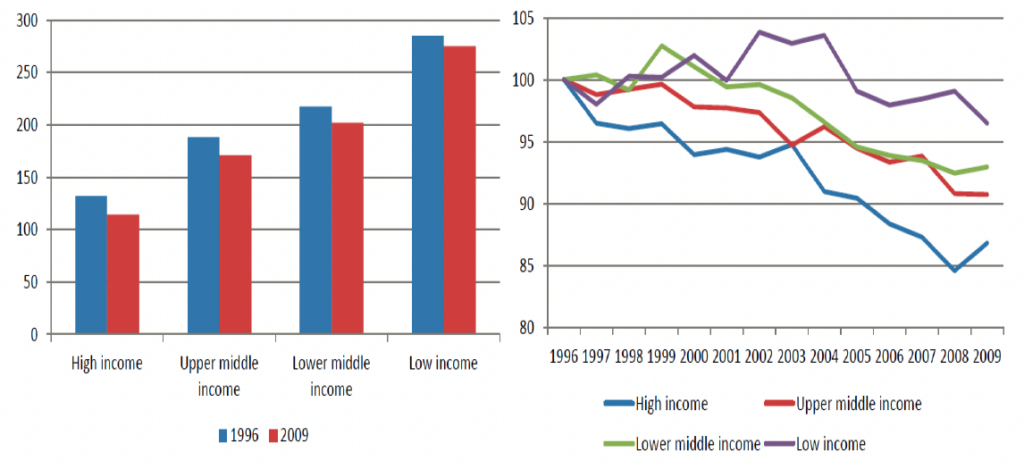

There is however substantial variation across countries and regions. The intensity in the participation of different parts of the world in what the authors hyperbolically call hyperglobalization is very unequal. Sub-Saharan African countries in particular remain heavily dependent on natural resources and agricultural products. Average trade costs remain much higher for low-income countries than richer countries, and in the last 15 years trade costs have fallen much more in the former than the latter, in part because of a lack of “connectivity” reflecting weaknesses in infrastructure (figure 1). Many countries in Africa as well as in South Asia, much of the Middle East, and the members of Mercosur in Latin America have not seen the shift toward intraindustry trade and participation in international supply networks that has been a driver of trade growth in East Asia, Mexico, Turkey, and Central and Eastern Europe and the emergence of what Richard Baldwin has called Factory Europe, Factory Asia, and Factory North America. As Dani Rodrik stresses in his paper for this project, from the perspective of the “average” global citizen, much therefore depends on location. Many countries are simply not participating in the global value chains and fragmentation of manufacturing production that underlies a large share of the growth in the value of gross trade flows. Fostering greater diversification and participation by African, Latin American, and Middle Eastern economies in international supply networks is one of the great challenges confronting governments of the countries concerned as well as the trading system.

Figure 1 Average Trade Costs for Manufactured Exports, by Income Group, 1996–2009

Note: The unit in the first panel is average trade costs as percentage ad valorem equivalents for the 10 largest importing partner countries for each country in the sample. The unit in the second panel is an index in which 1996 = 100.

Technological changes have had a massive impact in supporting the long boom in trade. Just-in-time, multicountry lean manufacturing would be impossible without the process innovations and ICT that permit supply chain management spanning hundreds of suppliers located in different countries. Baldwin’s (2011) “second unbundling” is not affecting only the production of industrial and high-tech products (as exemplified by the well-known examples of the Boeing airplane and the iPhone); it also has had enormous implications for firms producing basic consumer products. Walmart alone accounts for some 9 percent of U.S. imports of goods. However, as discussed below, much of the value that is embedded in U.S. imports is actually created in the U.S.

Technological advances increasingly are permitting greater “dematerialization” of trade. It may be surprising therefore that the share of services in global trade has been remarkably constant since the 1980s, at about 20–25 percent. What has changed is the composition of this trade, with private business services—which includes activities such as the business process outsourcing phenomenon—growing in importance and the share of travel and transport declining. The value of world trade in services has been expanding rapidly, but so has trade in goods. As a result, the overall ratio has not changed much. In the future, this ratio is likely to change, with potentially major implications for the tradability of white collar jobs (Jensen 2011). Outsourcing and offshoring are increasingly going to be a feature of the organization of production and trade and a determinant of productivity of firms. The trend toward the digitization of products to allow them to be created in one location and transmitted to another for processing or consumption could have major effects on the pattern and composition of trade. One example is the development of 3D printing, which has the potential to obviate the need to ship parts and components, which firms and consumers will “print” on demand. Such developments could have major impacts on trade flows and the pattern and composition of employment.

Although manufactures and services account for the lion’s share of global trade, it is important not to lose sight of agriculture, which remains of great significance for many low-income countries. Many rich countries subsidize and otherwise support the sector, creating negative spillovers for many of the poorest economies in the world (Anderson 2009). As Subramanian and Kessler argue, a concerted push is needed to reduce the use of distorting policies, including export restrictions by producers seeking to reduce domestic consumer prices for food staples. Higher food prices resulting from climate change and the expanding size of the global middle class can be expected to generate greater supply and have been beneficial for farmers and rural communities. But such supply responses in low-income countries will depend on both domestic policies and the existence of a level playing field. More generally, beyond agriculture, a key barrier for trade expansion for many firms in low-income countries is that notwithstanding duty-free access programs, the effective market access conditions that prevail are determined in (large) part by nontariff measures, including rules of origin. A major benefit of moving toward the elimination of tariffs on a most favored nation basis is that doing so eliminates the need for rules of origin, thereby greatly simplifying the life of traders and reducing trade costs.

China and the “Rise of the Rest”

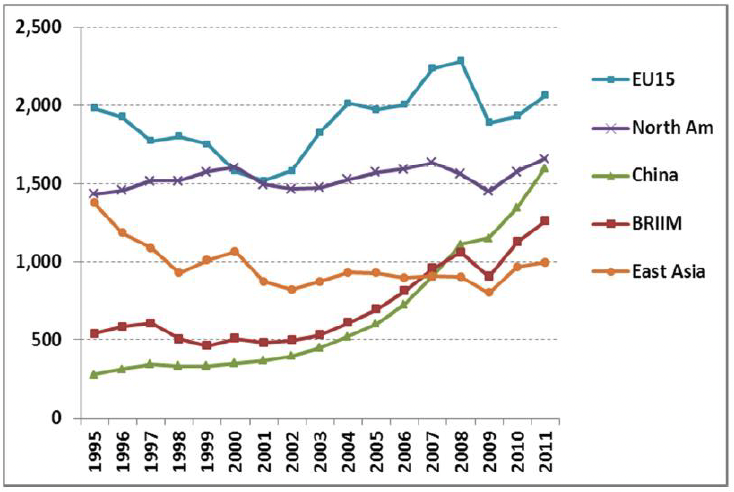

Subramanian and Kessler devote a significant part of their paper to the increasing share of world trade accounted for by China, which they define as a “mega-trader” because its trade to GDP ratio is much larger than what has been observed for other countries at similar stages of development in the past. It is not clear, however, that the magnitude of China’s gross trade flows is a variable that is of policy interest or concern. Underlying the flow of trade from China and other developing countries that are part of global production networks are large innovative companies that are often headquartered in the North and combine labor in different locations, supply chain management, and efficient logistics to provide their customers with a greater variety of products at lower cost. Much of this value originates at the up- and downstream ends of value chains and is created through services-related activities. Gross trade flows are therefore misleading. Of greater relevance is the extent to which China and other developing countries are generating value added. One stylized fact to note here is that in absolute terms, OECD countries have seen stagnating in the absolute amount of value added produced in manufacturing since the mid-1990s, while value added in the emerging markets has risen steadily. This is not just a China story (figure 2).

Figure2 Regional Contribution to Global Manufacturing Value Added, 1995–2011

(billions of 1995 dollars)

Note: East Asia includes Japan, the Republic of Korea, and Taiwan, China. BRIIM includes Brazil, Russia, India, Indonesia, Mexico, and Turkey. EU15 comprises the states that joined the European Union before 2004.

The authors stress China’s mercantilist policy stance and its resulting effect of generating current account surpluses (that is, ensuring that domestic savings exceed investment through financial repression) and imply that this stance has created negative spillovers for the United States and the rest of the world. Views differ on this matter. Underemphasized are the benefits that China’s growth has brought, not just in economic terms—in massively reducing poverty in one of the world’s most populous countries—but also in demonstrating that using the world economy to pursue and sustain a high growth path remains feasible for any country. The insertion of China into the world economy inevitably was going to impose adjustment pressures on the rest of the world.2 The process was arguably effectively managed by the Chinese authorities and has certainly not been all negative for other countries. Emphasizing the negative competitiveness effects of an undervalued Chinese currency on other countries neglects the positive effects of Chinese growth for consumers (the average citizen) around the globe and natural resource exporters in Africa, Latin America, and Central Asia. As real wages in China rise, outward foreign direct investment (FDI) flows will presumably increase, including in low-income countries.

2 The emergence of China as a major player following its reentry into the global economy is one element of a broader trend: the collapse of communism. The fall of the Iron Curtain also fostered the reintegration of Central and Eastern European countries with Western Europe. A good part of the increase in intraindustry, intraregional trade that occurred after1990 involved Europe. Integration of many of the former Comecon nations helped Europe maintain its external (global) market share in manufactures until the mid-2000s (Timmer and others 2013).

China is (still) the most populous country in the world, with 1.3 billion people, many of whom are relatively poor. It has made good use of the opportunities that exist through supply chains to put its people to work to satisfy demand in the rest of the world. The fact that China is a large trader is a reflection of initial conditions as well as its policies. What is much more relevant than China’s gross trade to GDP ratio is the sustainability of the trade-led development strategy it has so successfully pursued over the last 30 years. The big challenge confronting both China and the rest of the world is to manage the inevitable and desirable rebalancing of the Chinese economy toward greater reliance on domestic demand and to expand domestic employment in service sectors such as retail trade, domestic logistics, and leisure, health, and financial services.

Policy Challenges

Subramanian and Kessler identify three “pressing proximate challenges” (exchange rate undervaluation by major traders with large current account surpluses, World Trade Organization [WTO] rules that impede the use of “green” industrial policy, and the use of export restrictions for food and natural resources) as examples of the deeper, fundamental policy challenges that must be addressed in order to sustain an open global trade regime and support further globalization. Within countries a key focus, as emphasized by the authors, must be to maintain effective social insurance mechanisms and to ensure greater equality of opportunities through appropriate labor market and educational policies. Across countries the major near-term challenge is arguably to manage the adjustment of the large current account imbalances that prevail today.

China will play an important role in that adjustment process, but this matter extends to surplus countries other than China, such as Germany, the Nordic countries, oil exporters, as well as to countries with large current account deficits, such as the United States. Policies in the rest of the world matter as much as those pursued by China. The “savings glut” during the 2000s was no doubt in part the result of policy in China, but also important was the weak regulation and absence of policies in deficit countries to manage and productively allocate the capital outflow from China and other countries where savings (greatly) exceeded investment. Focusing on what are arguably symptoms or specific dimensions of this issue, such as China’s currency policy, is too narrow an approach.3 A key question looking forward is how the further structural transformation of the Chinese economy toward services and domestic consumption will be managed by the government and how it can be supported by the rest of the world. This process will offer significant opportunities for firms in OECD countries to provide services and could lead to greater interest in China in engaging in multilateral cooperation in the WTO. Rather than assume that China needs to be forced to pursue additional policy reforms, it should be recognized that further liberalization is in China’s self-interest and thus likely to be pursued autonomously in a number of areas, including in services.

3 Calling for the WTO to get involved in adjudicating disputes about the level of nominal exchange rates is not the way to go. Trade policy is not an appropriate tool with which to address monetary policy–related conflicts.One reason why this is so is that it is necessary to consider the overall current account and not bilateral trade balances. One deficit country taking trade action against a surplus country may not do much to affect the balance of overall imports and exports of the two countries concerned. More fundamentally, the level of the real exchange rate reflects a mix of fiscal and monetary policies that more often than not have nothing to do with trade policy objectives (Staiger and Sykes 2010).

Another major global policy challenge is to achieve greater participation by more developing countries in international production networks through diversification of their export structure. As noted by the authors and by Dani Rodrik in his paper for this project, meeting this challenge requires appropriate national policies, including, I would argue, further liberalization of trade in goods and services (such as air and road transport). But there is much that other countries can do to assist—by complementing duty-free access with simple and liberal rules of origin, by implementing regional integration agreements that provide better (lower cost) access to ports and airports, and by taking action to reduce the costs of compliance with regulatory standards, including through aid for trade.

The types of policy instruments that increasingly are (will be) the source of international spillovers and potential conflicts/disputes have changed. Traditional trade barriers, such as tariffs and quotas, are less and less a major factor; the policy agenda looking forward is largely one that addresses the spillover impacts of domestic “behind-the-border” regulatory policies and industrial policies (so-called nontariff measures); examples include product regulation, certification and conformity assessment procedures, licensing requirements for service providers, data reporting and privacy standards, and border management procedures. Many of these regulatory policies often apply equally to local and foreign firms and products, but they generally increase trade costs more for foreign than for domestic suppliers, simply because regulations differ across countries or because foreign firms are subject to a multiplicity of requirements that are redundant (duplicative). Such measures cannot be “negotiated away,” as presumably they fulfill a specific social or economic purpose that is not discriminatory in intent. Processes are needed that help build a common understanding of trade impacts and a search for mechanisms to reduce them without undermining the attainment of the underlying objective.

Two major challenges arise: determining how policies affect operating costs in general (that is, affect competitiveness) and determining the extent to which they distort trade. The goal should be to identify the policies that have the greatest impact on such costs and how international cooperation can reduce negative trade effects. There is no presumption that the WTO is necessarily the best forum in which to do this. PTAs or other forms of cooperation may dominate.

Prospects for International Cooperation

The authors lay out three possible scenarios for the future of the trade regime: liberalization (more globalization), maintenance of the status quo (preventing backsliding), and a retreat from globalization. If realized, they argue, each scenario will raise specific challenges that differ across different groups of countries. Which scenario will end up being realized is endogenous; presumably what we want to identify are the factors that may constrain the realization of the optimal scenario (which the authors argue is continued movement toward greater openness) and what could (should) be done to relax these constraints. However, much of what the authors discuss in terms of desirable (necessary) policies is not linked back to these three scenarios. In any event, it would appear that the policies that are needed to further liberalize trade and investment and to sustain an open world economy overlap to a great extent, so it is not clear how useful the three scenarios are in terms of providing insights into the likely path of the trade regime.

Facilitating a continued process of broad-based beneficial economic growth in the poorer countries of the world requires that the global trading system remain open and preferably that countries go further to liberalize trade. The global trade regime has provided an important framework for countries to agree to trade policy disciplines and commitments, as well as a mechanism through which these commitments can be enforced. The scope and coverage of multilateral policy rules has expanded steadily since the creation of the General Agreement on Trade and Tariffs (GATT), in 1947, as has membership, which now stands at 159 countries. Thirty-plus new members—all developing countries or economies in transition—have acceded to the WTO since it was established in 1995, and another 20 are in the process of negotiating accession. The popularity of the WTO is a stylized fact of the post-1990 period that deserves greater emphasis.

Trade agreements like the WTO are self-enforcing mechanisms through which countries can cooperate to internalize negative spillovers that are a large enough to matter. An important question is whether the WTO—that is, multilateral cooperation involving 159 economies— is the best mechanism to manage the (pecuniary) spillovers created by national policies. PTAs are an alternative mechanism. They have been a feature of national trade strategies of many countries for decades. What is significant is not so much the increase in the number of PTAs in recent years—many of which are not “deep,” in contrast to what is sometimes claimed, including by the authors, as they often do not go much beyond the WTO in key areas such as services trade policy (see, for example, Hoekman and Mattoo 2013)—but the fact that the United States decided to join the European Union and pursue PTAs with not only (small) developing countries but also other high-income countries. The European Union has always been a serial “offender” in this area—as of the mid-2000s European countries accounted for about half of all the PTAs notified to the WTO.4

It is unclear to what extent the shift to mega-regionals by the United States or a trade agreement between the European Union and the United States represents a threat to the trading system. There has been much speculation about the motivations of the United States in particular in pursuing specific PTAs, especially the Trans-Pacific Partnership (TPP). The extent to which its interest is motivated by China is arguably less important than is sometimes argued (Schott, Kotschwar, and Muir, 2013). Given the deadlock in the Doha Round, a positive implication of the many PTAs in force and under negotiation is that they are a signal that governments remain willing to make binding trade policy–related commitments in treaty-based instruments. The pursuit of mega-regionals reflects the fact that the countries involved cannot “get to yes” in the WTO, because, as the authors note, the negotiating set that is currently offered in the WTO is too small. The Doha Round has centered largely on market access issues, where there are large asymmetries in the average levels of protection that prevail in the markets of the major protagonists—the European Union/United States on the one hand and China/India on the other. At the same time, many important policy areas that create large negative spillovers are not on the table (export restrictions are an example).

It is not at all obvious that killing off the Doha Round and launching a new “China Round” will make a difference in this dynamic. A number of the policies for which the European Union and the United States would like to negotiate disciplines are going to be difficult to agree on (for example, the role of state ownership of companies, industrial policies, and government procurement). The fundamental constraint that is precluding the Doha Round from being concluded—namely that the United States and the European Union have little to offer—continues to apply. The same reasoning suggests that the extent to which the “mega-regionals” will put “pressure” on countries such as Brazil, China, and India to come to the negotiating table may be limited. Much will depend on the extent to which negotiations result in economically meaningful outcomes and the degree to which these outcomes imply discrimination against products coming from nonparties. Classic trade diversion costs generated by preferential liberalization are likely to be small, because average tariffs in most of the participating countries are low. There may be greater potential for de facto discrimination resulting from measures that have the effect of reducing the market segmenting effects of differences in regulatory policies. But even here much depends on whether third-country firms will be able to benefit from access to the larger market created by the PTA if they are able to demonstrate compliance with the relevant regulatory standards. In practice, it may be difficult to exclude third-country firms from benefiting from initiatives that lower the fixed costs associated with enforcement of regulation in member countries.

4 The proliferation of PTAs signed by East Asian countries starting in the late 1990s was more a reaction to than a driver of intraindustry, intraregional trade and investment flows. The evidence suggests that Asian PTAs have had virtually no impact on the pattern and growth of trade (Menon 2013).

The challenge for the vast majority of WTO members that are excluded from the mega-regionals is to identify actions that can be taken to reduce potential downsides and/or to benefit from these initiatives. One response is for excluded countries to pursue PTAs themselves, which has already been happening. Such agreements can help increase trade with a set of countries that is growing more rapidly than the European Union and the United States and in which traditional barriers to trade are substantially higher. If such PTAs result in meaningful preferential liberalization, the associated trade diversion could become an incentive for a renewed effort to conclude a multilateral deal, which might also become more feasible than it is today by eroding the power of the interest groups in the BRICS that currently resist market opening on a most favored nation basis.

Given that classic diversion costs from the mega-regionals are likely to be limited and that their (proclaimed) goal is to be high-quality, “21st century” agreements that address the regulatory causes of market segmentation and reduce the cost-raising effects of prevailing domestic policies, one response is to focus resources on evaluating these PTAs and understand what they do. The new PTAs are a learning opportunity, not just for countries that are members but also for countries that are not. Over time, WTO members may determine that embedding some of the processes and approaches that have proved successful in a PTA context into the WTO makes sense. A precondition for such learning and “technology transfer” is information: WTO members need to invest in understanding what is being done in the PTA context. The WTO can be used for this purpose.

Another response to the proliferation of PTAs is to consider what can be done to reduce the incentive to use the PTA route for countries that want to go beyond existing WTO disciplines and to multilateralize specific features of the PTAs that are effective in reducing regulatory trade costs. The WTO allows for so-called plurilateral agreements among a subset of its members that apply only to signatories. Given that much of the “21st century” trade agenda concerns regulation, there should arguably be greater flexibility and willingness by the WTO membership to allow countries to pursue cooperation on such matters inside the WTO rather than effectively forcing countries to use PTAs. Doing so would not only help reduce the fragmentation of the trading system over time, it would also increase global welfare for average citizens by providing a vehicle for all WTO members to benefit from the initiatives and experimentation that is going to be pursued in the context of PTAs.

On balance, strong forces are likely to sustain the process of international specialization and fragmentation of production that has been a driver of trade growth in recent decades. One of these forces is the fact that international production networks require low trade costs in order to operate. One reason why there was no major increase in trade barriers after the 2008 global financial crisis was that firms in countries that are most involved in supply chain trade did not ask for them, as trade protection would not have helped them. Trade is likely to continue to be an engine of growth and global poverty reduction over the next decade or two if more low-income countries become part of the international supply chains that produce manufactures. For them to do so, they must reduce trade costs, through a mix of national action and international cooperation, and the process of current account rebalancing and adjustment must be managed well. Whatever the prospects for growth in the near term—and they are not bright in Europe and likely to be lower than they were in previous decades for all countries—technological and environmental changes will continue to affect the pattern and composition of trade. These changes will not necessarily imply ever greater offshoring. As is already being observed, changes in technologies and the rising costs of offshoring and operating supply chains will also result in reshoring, the shortening of supply chains, and the “greening” of logistics and transport services (see, e.g., World Economic Forum, 2013).

References

- Anderson, K., ed. 2009. Distortions to Agricultural Incentives: A Global Perspective, 1955–2007. Washington DC: Palgrave-McMillan and World Bank.

- Arvis, J. F., Y. Duval, B. Shepherd, and C. Utoktham. 2013. “Trade Costs in the Developing World: 1995–2010.” World Bank Policy Research Working Paper 6309, Washington, DC.

- Baldwin, R. 2011. “Trade and Industrialisation after Globalisation’s 2nd Unbundling: How Building and Joining a Supply Chain Are Different and Why It Matters.” NBER Working Paper 17716, National Bureau of Economic Research, Cambridge, MA.

- Hoekman, B., and A. Mattoo. 2013. “Liberalizing Trade in Services: Lessons from Regional and WTO Negotiations.” International Negotiation 18: 131–51.

- Jensen, J. B. 2011. Global Trade in Services: Fear, Facts, and Offshoring. Peterson Institute for International Economics, Washington DC.

- Kee, H. L., A. Nicita, and M. Olarreaga. 2009. “Estimating Trade Restrictiveness Indices.” Economic Journal 119 (534): 172–99. 13

- Menon, J. 2013. “Supporting the Growth and Spread of International Production Networks in Asia: How Can Trade Policy Help?” ADB Working Paper on Regional Economic Integration 114, Asian Development Bank, Manila.

- Schott, J., B. Kotschwar, and J. Muir. 2013. Understanding the Trans-Pacific Partnership. Peterson Institute for International Economics, Washington DC.

- Staiger, R., and A. Sykes 2010, “Currency Manipulation’ and World Trade.” World Trade Review 9 (4): 583–627.

- Timmer, M. A. Erumban, B. Los, R. Stehrer, and G. de Vries. 2013. “Slicing Up Global Value Chains.” GGDC Research Memorandum 135, Groningen Growth and Development Centre, University of Groningen, the Netherlands. http://www.ggdc.net/publications/memorandum/gd135.pdf.

- World Economic Forum. 2013. Outlook on the Logistics & Supply Chain Industry 2013. Global Agenda Council on Logistics & Supply Chain Systems 2012-2014, Geneva: WEF.

- WTO (World Trade Organization). 2007. World Trade Report 2007: Six Decades of Multilateral Trade Cooperation. Geneva: WTO.

- ———. 2012. International Trade Statistics 2012. Geneva: WTO.