The Hyperglobalization of Trade and Its Future

Arvind Subramanian and Martin Kessler

Abstract

The open, rules-based trading system has delivered immense benefits—for the world, for individual countries, and for average citizens in these countries. It can continue to do so, helping today’s low-income countries make the transition to middle-income status. Three challenges must be met to preserve this system. Rich countries must sustain the social consensus in favor of open markets and globalization at a time of considerable economic uncertainty and weakness; China and other middle-income countries must remain open; and mega-regionalism must be prevented from leading to discrimination and trade conflicts. Collective action should help strengthen the institutional underpinnings of globalization. The world should move beyond the Doha Round dead to more meaningful multilateral negotiations to address emerging challenges, including possible threats from new mega-regional agreements. The rising powers, especially China, will have a key role to play in resuscitating multilateralism.

Key words:

Hyperglobalization, trading system, mega-regionalism, mega-trader, China, criss-crossing globalization, foreign direct investment

WORKING PAPER 3

JUNE 2013

Global Citizen Foundation

Phone: +41 (0) 225 18 0265

e-mail: info@gcf.ch

The Hyperglobalization of Trade and Its Future

Arvind Subramanian and Martin Kessler

1. Introduction

The post–World War II period witnessed a rapid rise in trade between nations, reminiscent of the integration that occurred before World War 1 (see WTO forthcoming; Krugman 1995). This evolution was facilitated partly by reductions in policy barriers—first in the advanced economies, under the auspices of the then General Agreement on Trade and Tariffs (GATT), and later in developing countries, through unilateral liberalization actions or under programs with the International Monetary Fund (IMF) and World Bank. Trade was also facilitated by technological advances, especially in shipping and transportation costs. By the end of the 1980s and early 1990s, global trade integration had reverted to levels last seen before World War I.

The postwar period also saw a number of growth successes, beginning with Japan (and Europe), followed by the East Asian tigers and then China and more recently by India. Along the way, a few countries in Sub-Saharan Africa and Latin America also succeeded in raising their standards of living.

In the late 1990s, however, a striking change occurred in the economic fortunes of countries: economic growth took off across the world, a phenomenon that is best described as convergence with a vengeance. Until the late 1990s, only about 30 percent of the developing world (21 of 72 countries) was catching up with the economic frontier (the United States), and the rate of catch-up was about 1.5 percent per capita per year (table 1.1).1 Since the late 1990s, nearly three-quarters of the developing world (75 of 103 countries) started catching up, at an accelerated annual pace of about 3.3 percent per capita. Although developing country growth slowed during the global financial crisis (2008–12), the rate of catch-up with advanced countries was not materially affected and remained close to 3 percent (see also Rodrik’s paper on this website).

Arvind Subramanian is a senior fellow at the Peterson Institute for International Economics and the Center for Global Development. Martin Kessler is a research analyst at the Peterson Institute. The authors are grateful to the project’s participants, including Richard Baldwin, Nancy Birdsall, Kemal Derviş, Shahrokh Fardoust, Theophilos Priovolos, Dani Rodrik, and Andrew Steer, and their colleagues at the Peterson Institute for International Economics and the Center for Global Development for helpful discussions. This paper draws on work with Aaditya Mattoo and on Subramanian (2011). This paper was prepared for the Towards a Better Global Economy Project funded by the Global Citizen Foundation. The authors alone are responsible for its content. Comments or questions should be directed to asubramanian@piie.com.

1 All growth figures in this paragraph use a GDP measure in purchasing power parity (PPP) terms.

Table 1.1 Convergence: Growth of Developing Countries Compared to with Growth in the United States

| Indicator | 1870–1960 (Maddison) | 1960–2000 (Penn World Tables 7.1) | 2000–07 (Penn World Tables 7.1) | 2000–11 (World Development Indicators) | 2008–12 (World Economic Outlook) a |

|---|---|---|---|---|---|

| U.S. growth rate of GDP per capita (percent) | 1.7 | 2.47 | 1.28 | 0.65 | 0.02 |

| World growth rate of GDP per capita (percent) | 1.3 | 2.75 | 3.17 | 2.28 | 1.73 |

| Number of developing countries in which growth exceeded U.S. rate | 2 | 21 | 75 | 80 | 78 |

| Percentage of developing countries in which growth exceeded U.S. rate | 5.3 | 29.2 | 72.8 | 89.9 | 83.9 |

| Average excess over U.S. growth (percentage points)b | 0.02 | 1.53 | 3.25 | 2.94 | 3.03 |

| Number of countries in sample | 38 | 72 | 103 | 89 | 93 |

Note: Sample excludes oil exporters (as defined by the IMF) and countries with populations of less than 1 million.

a. Based on GDP in constant dollars. Other columns use GDP in PPP terms.

b. Computed as simple average growth of countries whose growth exceeds that of the United States.

At around the same time, perhaps just preceding this convergence phase, world trade started to surge, ushering in an era of hyperglobalization. That rising globalization (hereafter used interchangeably with trade integration) is associated with stronger growth, which is a prerequisite for improving the situation of average citizens all over the world, is reason enough to seek to sustain it. This integration need not continue at the torrid pace of recent years; it should be sustained at a relatively steady rate and any serious reversal, which could set back the prospects of the average global citizen, avoided.

This paper is divided into six sections. The next section documents some of the salient features of this era of hyperglobalization. Section 3 discusses three key areas where the trading system is seen as inadequate. The problems are illustrative of the proximate challenges and possible solutions, but in important ways, they cannot be solved unless the more fundamental challenges of globalization are addressed. Section 4 explores these deeper challenges. Section 5 suggests possible policy responses at the national and international levels that could help sustain globalization. Section 6 offers brief concluding remarks.

The paper is not comprehensive: it focuses on the trade aspects of globalization. It does not discuss other important forms of globalization relating to the movement of finance and people. Rather, it focuses on the major challenges, emphasizing aspects and arguments that have perhaps received less attention thus far.2

2. Seven Important Characteristics of the Most Recent Wave of Globalization

This section describes seven major features of the current era of hyperglobalization and of today’s trading system:

- hyperglobalization (the rapid rise in trade integration)

- the dematerialization of globalization (the importance of services)

- democratic globalization (the widespread embrace of openness)

- criss-crossing globalization (the similarity of North-to-South trade and investment flows with flows in the other direction)

- the rise of a mega-trader (China), the first since Imperial Britain

- the proliferation of regional trade agreements and the imminence of mega-regional ones

- the decline of barriers to trade in goods but the continued existence of high barriers to trade in services

2 For this reason, notable features such as the decline in transportation costs and improvements in information and communication technologies, which have been widely noted, are not studied in depth here (for discussions of these issues, see WTO 2013).

Hyperglobalization

Since the early 1990s, the world has entered into an era of what might be called hyperglobalization (figure 2.1). The years between 1870 and 1914 have been described as the first golden age of globalization. World trade as a share of gross domestic product (GDP) surged from 9 percent in 1870 to 16 percent on the eve of World War I. This was the era that Keynes waxed eloquently about, noting that an inhabitant of London “could order by telephone, sipping his morning tea in bed, the various products of the whole earth, in such quantity as he might see fit, and reasonably expect their early delivery upon his doorstep” (Keynes 1920, p.11).

Figure 2.1 World Exports, in Current Dollars, 1870–2011

The period between 1914 and the end of World War II witnessed the Great Reversal of globalization, as the combustible mix of isolationism, nationalism, and militarism ignited protectionist policies. World trade plunged to a low of 5.5 percent of world GDP just before World War II began (O’Rourke and Williamson 1999; Frieden 2006; Irwin 2011).

A third era, starting after World War II, saw the restoration of world trade, aided by declines in transport costs and trade barriers. Only by about the mid- to late 1970s did world trade revert to the peaks seen before World War I.

The world is now in a fourth era, of hyperglobalization, in which world trade has soared much more rapidly than world GDP. Merchandise exports-to-GDP ratios soared from 15 percent to 26 percent, and goods and services exports to about 33 percent 3, over the course of the last two decades. This rapid increase is somewhat surprising, because transport costs do not appear to have declined as rapidly as in earlier eras (Hummels, Ishii, and Yi 2001; Baldwin 2011a). The cost of information and communications did decline significantly, however.

Part of the increase in trade reflects the fragmentation of manufacturing across borders—the famous slicing up of the value-added chain—as individual production stages are located where the costs of production are lowest. This phenomenon, whereby technology no longer requires that successive stages of manufacturing production be physically contiguous or proximate, has been dubbed the “second unbundling” (Baldwin 2011a).4

This real technological impetus to trade tends to artificially inflate recorded trade. Because value is added at each stage of the production chain, it is recorded as exports at successive links in the chain. Gross exports flows therefore overstate real flows of valued added (exports net of imported intermediate goods). Figure 2.1 shows that, even though value added–based exports of goods and services are about 5 percentage points lower than exports measured on a gross basis, their trajectory has been similar to that of conventionally measured exports. More recently, value added as a share of exports has not declined substantially or across all trading regions (Hanson 2012; WTO 2013).5

3 Throughout this paper, we use trade data as currently measured, on a gross basis. Wherever possible, and as a cross-check, we also present results for trade data measured on a value-added basis. The appendix explains how these values are calculated.

4 The first unbundling reflected in the quotation from Keynes is the separation of the producer from the consumer that increased trade permits.

5 Koopman, Wang, and Wei (2013) further refined the measurement of value-added trade by distinguishing where countries are (upstream versus downstream) in the value-added chain. The aggregate value-added measures reported here are computed as in their paper.

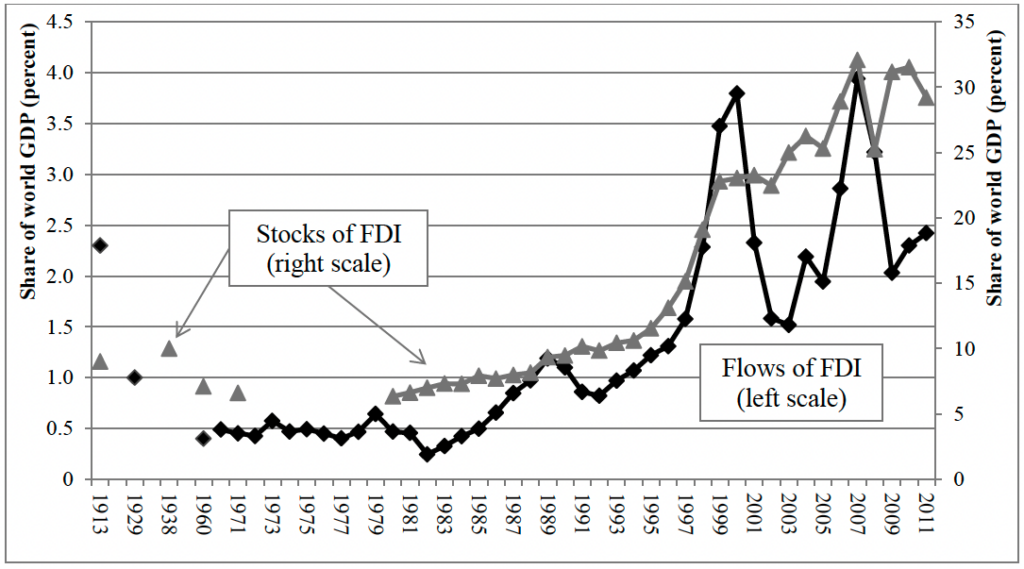

Figure 2.2 Stocks and Flows of Foreign Direct Investment, 1913–2011

A related feature of this era of hyperglobalization is the rise of multinational corporations and the sharp surge in flows of foreign direct investment (FDI), which have both caused and been caused by cross-border and other flows of goods and services. Since the early 1990s (broadly coinciding with the era of hyperglobalization), FDI flows have surged, growing substantially faster than GDP (figure 2.2). Global FDI as a share of world GDP, which hovered around 0.5 percent, increased sevenfold, peaking at close to 4 percent just before the onset of the recent global financial crisis. Even discounting the two surges of 1997–2000 and 2005–08, the general trend is steadily increasing. Global FDI stocks (which are less volatile than flows) jumped from less than 10 percent of GDP in the early 1990s to 30 percent in 2011. FDI flows, and stocks, now surpass levels achieved in the first golden era of globalization, before World War I. By 2009, there were more than 80,000 multinationals, accounting for about two-thirds of world trade (UNCTAD 2010).

“Dematerializing” Globalization

The rapid increase in trade has occurred in both goods and services. Based on conventional (gross) trade data, services trade represented about 17 percent of world trade in 1980 and about 20 percent in 2008. Measured in value-added terms, the corresponding numbers are 30 percent and 40 percent. The apparent paradox that we seek to explain in this section is that services trade, which represents 6 percent of world GDP in gross terms, is 40–50 percent larger when computed in value added terms. This phenomenon arises because services are not always directly tradable but are sometimes embodied in the production of goods that are traded. In traditional trade statistics, such services are not counted as traded; in value added terms, they are considered as such, because production of the service takes place in one country and consumption in another one. Traditional measures of services trade underestimate their importance in global trade.

Two underlying factors can explain the “dematerialization” of trade. First, as Johnson and Noguera (2012) show, the ratio of value-added exports to gross exports in manufacturing goods decreased in the last 30 years (from 60 percent in 1980 to 45 percent in 2009), as a result of the rising importance of global value chains in this sector. Second, as explained in the previous paragraph, trade in services is larger and growing faster in value added terms than traditional statistics show. Soon, trade in services could eclipse trade in goods, less because services are traded directly than because services are increasingly embodied in goods. Trade will actually be dematerializing—moving from “stuff” to intangibles—although the manifestation will be, and the data will record, the opposite effect.

Value added–based trade data reveal how much of total value added in a sector is traded globally. Figure 2.3 plots world exports (gross and value added) of goods as a share of world value added in goods (defined to include agriculture and industry), as well as similar numbers for services. During the period of hyperglobalization, value added exports of goods as a share of total value added in the sector (agriculture and industry) increased from about 33 percent to 47 percent, and services as a share of value added in the services sector increased from 11 percent to 16 percent. Thus, the pace at which services are becoming tradable mirrors that in merchandise.

Figure 2.3 Global Tradability of Goods and Services, 1975–2010

The slower rise in the tradability of goods than services in the era of hyperglobalization may partly reflect the differential rise in the costs of transport versus information and communications technologies (ICT). After plummeting sharply between about 1940 and 1980, transport costs appear to have stabilized (Baldwin 2011; Hummels 2007). In contrast, about 1990, the use of ICT–related technologies and applications surged. A consequence could have been a differential fillip to more sophisticated goods and especially services.

Democratic Globalization

Part of the increase in trade also reflects convergence and the wider distribution of output and income: that is, trade has grown because output has become more widespread and “democratic.” 10

Basic gravity theory implies that smaller countries tend to trade more than larger ones.6 A world of two equal-size countries will experience more trade than a world in which the larger country accounts for 95 percent of world output. Over time, the world is becoming less unequal in terms of the distribution of the underlying output that generates trade.7 For example, between 1970 and 2000 the world was constituted by about 7.0–7.5 country equivalents (with fluctuations) (figure 2.4).

Figure 2.4 Dispersion of World Output and World Exports, 1970–2010

Note: Country-equivalents are computed as = 1/Σsi2 , where si is the share of each country in world output. A higher number denotes a more equal distribution of output.

6 The gravity model of trade is theoretically well established and empirically validated. It shows that trade between two countries is proportional to their economic size and inversely proportional to their distance. Other things equal, a large country will trade more than a small one but will be less open (trade/GDP will be smaller).

7 As Anderson (2011) shows, in a world without trade frictions, the share of trade in world output is given by 1 – Σjbj2 where bj is the share of a country in world output. Inverting the expression gives the number of country-equivalents in the world, which increases with convergence. Baier and Bergstrand (2001) find a statistically significant effect of convergence on trade.

Since 2000, as more countries have started catching up with the rich, world output has become more dispersed: today, it is as if there were 10 country-equivalents in the world. In the era of hyperglobalization, roughly a third of the increase in trade can be accounted for by this democratization of world output (figure 2.4).

Figure 2.5 Trade Openness, 1870–2010

Note: For 1870–1950, openness is defined using Maddison’s measure of current exports in dollars (deflated by the US consumer price index) and Maddison’s GDP data. For 1951–2010, openness is the variable openk (Penn World Table 7.1) divided by 2. Oil exporters and small countries (populations of less than 1 million) are excluded.8

8 We chose the openk variable because it is the most comparable with the Maddison (pre–World War II) GDP data in that both are in constant purchasing power parity dollars. For the pre-War export data, there are two options for deflation: a measure of general U.S. inflation (for example, the consumer price index [CPI]) or a measure of export prices. Maddison provides a real export series based on the latter. We chose the CPI option for the simple reason that the estimates for 1950 matched better the pre–World War II estimates for the years close to 1950. If we use Maddison’s real export data, the changes over time are even more dramatic than shown in figure 2.4 (that is, export-to-GDP ratios are lower for the past when exports are deflated by an export price index than a CPI index).

Even if the rise in world trade is caused by spreading prosperity, is this rise itself broadly spread? The numbers in figure 2.1 are in effect a GDP–weighted average of individual country’s export-to-GDP ratios. We can, instead, calculate export-to-GDP ratios that are unweighted or weighted by population to measure the reach of globalization across countries and across people, as done in figure 2.5.

Figure 2.5 shows that in 1913, the peak of the first golden era of globalization, the unweighted average export-to-GDP ratio in the world was close to 15 percent. In 2010, it was 21.5 percent. The population-weighted export-to-GDP ratio was about 6 percent; by 2010, it was 15 percent. Hyperglobalization has thus come about not just because some rich countries are becoming more open but also because openness is being embraced more widely.9 Keynes’ paean to globalization was thus both imperialist and elitist.10, 11

Criss-Crossing Globalization

Trade has been increasing steadily. But one of the unique features of the most recent phase of hyperglobalization is the fact that similar kinds of goods (and capital) are criss-crossing global borders. In other words, it is less and less the case that a country’s imports and exports are very different.

Three manifestations of such criss-crossing globalization can be discerned. In the immediate aftermath of World War II, the industrial countries increasingly started to export and import manufactured goods (for example, Japan, Germany, and the United States all exported and imported cars), a phenomenon at odds with classic Ricardian model. Models of monopolistic competition (Helpman and Krugman 1985) combined with consumers’ love for variety (differentiated products) provided the theoretical basis for the phenomenon of intraindustry trade that related to trade in final goods. Melitz and Trefler (2012) show that the share of intraindustry trade in total trade increased by nearly 20 percentage points. But this increase occurred between 1960 and the mid-1990s rather than over the most recent period of hyperglobalization. In fact, since the 1990s, this share of intraindustry trade has stabilized (Brulhart 2008).

9 One potential problem with figure 2.5 is that the sample is not constant over time. The finding that trade has become more democratized holds even for the constant sample of countries (not reported here). The unweighted average is above the population-weighted average because populous countries tend to trade less.

10 Even within the United Kingdom, the benefits of globalization were not broadly accessible. In 1912, for example, there were 0.6 million telephone subscribers in the United Kingdom, the population of which was about 46 million.

11 Another way of describing this democratization is to note that the trade of low- and middle-income countries has grown more rapidly than their incomes and more rapidly than the trade of high-income countries and that a bulk of this growth is trade among low- and middle-income countries (Hanson 2012).

For the rapidly growing emerging market countries of Asia, criss-crossing globalization has taken the form of greater two-way flows of parts and components than of final goods. This phenomenon is related to the slicing up of the value-added chain and the unbundling noted above.

The share of parts and components in trade offers one measure of criss-crossing globalization. For the world as a whole, this share increased from about 22 percent in 1980 to 29 percent in 2000. Since then, intermediate goods trade declined to about 26 percent of total trade, suggesting that the internationalization of production may have peaked (WTO 2013). Indeed, this form of globalization was really observed only in Asia, and even there intermediate trade has declined since 2000. Even in China, reliance on imports has declined markedly. In the computer sector (broadly defined), for example, exports were only 1.6 times imports in 1994, indicating substantial intermediate trade; by 2008, this ratio had climbed to 4.2 (Hanson 2012).

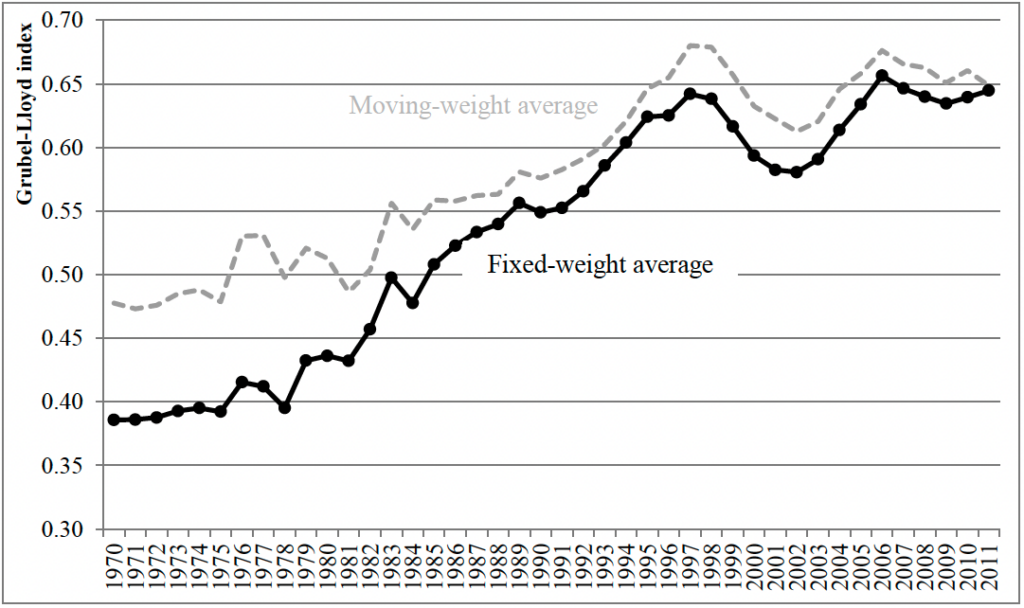

The third (and perhaps least remarked on) dimension of criss-crossing globalization, with potentially important effects for globalization policies, relates to two-way flows of FDI. It is one of the unique aspects of this era of hyperglobalization that developing countries (especially the larger ones) are exporting FDI (which embodies sophisticated factors of production, including entrepreneurial and managerial skills and technology)—and not just to other developing or countries (Mattoo and Subramanian 2010). Figure 2.6 plots a Grubel-Lloyd index of two-way flows of FDI at the global level.12 Depending on the weighting, this index climbed from about 0.3 in 1970 to almost 0.7 by 2011.

Figure 2.6 Two-Way Foreign Direct Investment Flows, 1970–2011

Note: The Grubel-Lloyd index is computed for each country with nonzero positive flows. Each country is then weighted by its share of total FDI flows, either with weights correspond to the current year (dotted line) or with weights that are fixed at their mean over the period (solid line). The figure shows five-year moving averages (to avoid large spikes).

The Rise of a Genuine Mega-Trader: China

When Krugman (1995) surveyed the evolution of world trade, he noted as one of the distinctive features the rise of a number of Asian super-traders, including Singapore, Hong Kong (China), and Malaysia, all of whose exports exceeded 50 percent of GDP, a feature never seen in the first era of globalization (in 1913, the United Kingdom’s ratio of export to GDP was 18.5 percent). But mega-traders can be defined in two senses: globally (relative to world trade) and nationally (relative to a country’s own output). Krugman clearly applied the latter criterion. Had he applied the former, one mega-trader he would have identified would have been Japan in the 1980s, which accounted for about 7.5 percent of global trade at its peak. Based on this criterion, none of the other East Asian Tigers would have been noteworthy, despite their astonishing performance: the small economies of Singapore, Hong Kong (China), Taiwan (China), and Malaysia accounted for a very small share of world trade at their peaks.

12 The Grubel-Lloyd index, which can take values between 0 and 1, measures the degree of two-way flows for a given country or industry. An index of 0 denotes that a country’s exports and imports are perfectly dissimilar—that is, a country is either fully an importer or an exporter of a good (or, in this specific case, a type of capital flow). An index of 1 denotes that a country’s exports and imports are similar—that is, a country exports and imports of a certain good are identical in magnitude.

Since 1990, a true mega-trader has emerged, China. It qualifies as such under both definitions of the term. Its integration into world trade accelerated with its accession to the WTO in 2001, transforming it into the world’s largest exporter and importer of manufactured goods, having surpassed the United States in 2012 (table 2.2).

Table 2.2 Merchandise Exports as Share of World Exports by Mega-Traders, 1870–2030

(percent)

| (percent) Year | United Kingdom | Germany | United States | Japan | China |

|---|---|---|---|---|---|

| 1870 | 24.3 | 13.4 | 5.0 | 0.1 | 2.8 |

| 1913 | 18.5 | 18.0 | 9.0 | 0.8 | 2.0 |

| 1929 | 15.1 | 16.6 | 14.4 | 2.1 | 3.0 |

| 1950 | 10.2 | 3.9 | 16.2 | 1.3 | 0.9 |

| 1973 | 5.1 | 12.9 | 12.2 | 6.4 | 1.0 |

| 1990 | 5.3 | 12.0 | 11.3 | 8.2 | 1.8 |

| 2000 | 4.4 | 8.5 | 12.1 | 7.4 | 3.9 |

| 2012 | 2.6 | 7.7 | 8.4 | 4.4 | 11.2 |

| 2020 (projected) | 1.9 | 5.3 | 8.8 | 3.9 | 12.1 |

| 2030 (projected) | 1.4 | 3.6 | 7.3 | 3.2 | 15.0 |

China’s exports as a share of GDP are now almost 50 percent. When its size and income level are taken into account, it is a substantial over-trader, comparable to the United Kingdom in the heyday of its empire and a vastly bigger trader than the United States, Japan, or Germany at their peaks.

For example, in 1975, the United States’ trade-to-GDP ratio was 13.3 percent (table 2.3). Given the size and income level of the United States, that number represented under-trading of about 50 percent. Japan in 1990, with a trade-to-GDP ratio of 20 percent, under-traded by about 50 percent. In contrast, China’s trade-to-GDP ratio in 2008 was 56.5 percent, which represented over-trading of nearly 75 percent. Only Imperial Britain was a mega-trader in both senses of the term. In 1913, its exports represented 18.5 percent of world exports. Its export-to-GDP ratio was 12 percent, which represented over-trading of about 84 percent. China is thus the first mega-trader since Imperial Britain.

Table 2.3 Exports and Imports as Percent of GDP in Selected Mega-Traders

(trade as percent of GDP) Percent over-trading, controlling for key gravity variables

| Item | Actual | Controlling for size | Controlling for size and income level | Controlling for size, income level, and oil-based economies |

|---|---|---|---|---|

| United Kingdom 1870 (sample includes 26 countries) | ||||

| Exports | 12.2 | 339.3*** | 84.0* | n.a |

| United States 1975 (sample includes 121 countries) | ||||

| Exports | 8.5 | –9.5 | –37.0*** | –36.3*** |

| Imports | 7.6 | –30.5*** | –37.7*** | –37.5*** |

| Total trade (exports + imports) | 16.1 | –20.9*** | –35.5*** | –35.1*** |

| Japan 1990 (sample includes 131 countries) | ||||

| Exports | 10.3 | –33.8*** | –56.8*** | –55.6*** |

| Imports | 9.4 | –44.3*** | –49.4*** | –51.4** |

| Total trade (exports + imports) | 19.7 | –40.4*** | –52.9*** | –53.7*** |

| China 2008 (sample = 136 countries) | ||||

| Exports | 35.0 | 79.9*** | 68.6** | 80.5*** |

| Imports | 27.3 | 45.7*** | 46.2*** | 38.0** |

| Total trade (exports + imports) | 62.2 | 64.6*** | 60.8*** | 62.0*** |

Sources: Maddison for United Kingdom; IMF various years and Penn World Table 7.1 for all other countries.

Note: All coefficients were obtained by running a regression of exports, imports, trade on column heads a plus dummy for the country in question. The level of over-/under trading is exp(dummy coefficient) – 1. A negative value denotes under-trading. * = significant at the 10 percent level, ** = significant at the 5 percent level, *** = significant at the 1 percent level.

If trade continues to grow in line with income, China’s dominance in world trade will become even greater. According to simple calculations in Subramanian (2011), by 2030 China could account for about 16–17 percent of world exports, nearly three times the share of the United States (see table 2.2).13 Even at the height of U.S. dominance, around 1975, it did not account for as large a share of world trade or have as great an edge over its nearest competitors (in 2000, the United States accounted for about 16 percent of world exports compared with 8 percent for Germany and about 7 percent for Japan). Any discussion of trade and the trading system going forward must recognize this development (discussed further below).

Growing Regionalization, Preferential Trade, and Impending Hyperregionalization

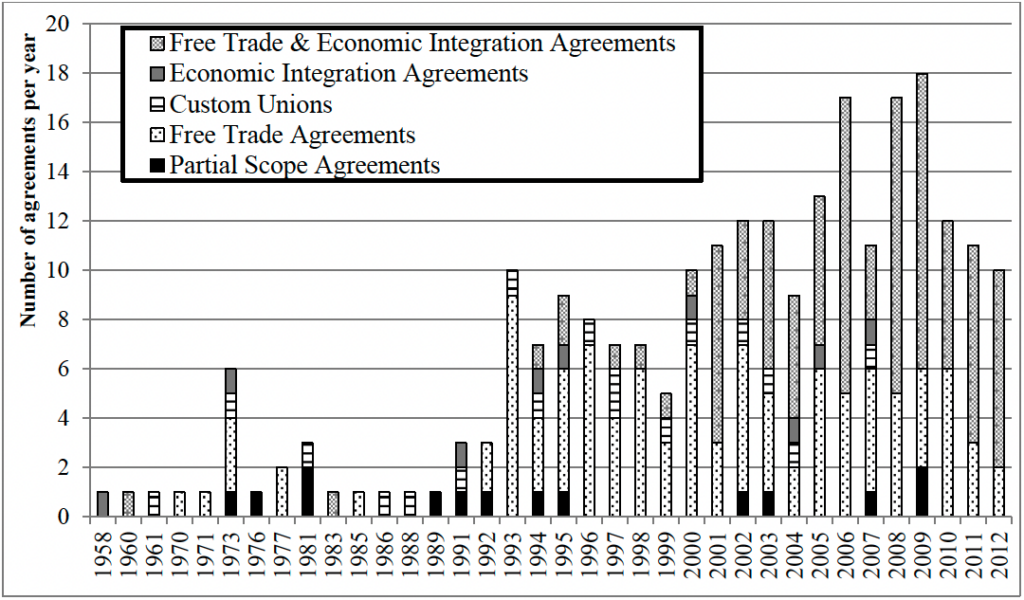

The era of hyperglobalization has been accompanied by a proliferation of preferential trade agreements (PTAs). Today, about half of the exports of the top 30 exporters go to preferential trade partners. Between 1990 and 2010, the number of PTAs increased from 70 to 300 (figure 2.7). In the mid-1990s, about 75 percent of PTAs were regional; by 2003, this share had dropped to about 50 percent. All World Trade Organization (WTO) members except Mongolia have concluded at least one PTA; some, such as the European Union, Chile, and Mexico, have concluded more than 20. Some of the large traders have already concluded agreements with each other or are about to do so (examples include the European Union and Mercosul, Japan and Mercosul, the European Union and India, and India and Japan).

The fact that nearly half of world trade is covered by preferential agreements does not mean that a comparable figure enjoys preferential barrier reductions. Carpenter and Lendle (2010) estimates that only about 17 percent of world trade is eligible for preferences; the remaining 83 percent either enjoys zero nondiscriminatory tariffs (nearly 50 percent) or is excluded from preferential agreements. Moreover, where preferences can apply, margins are low. For example, less than 2 percent of world imports enjoy preferences greater than 10 percentage points.

13 The WTO (2013) projection for 2035 is exactly in line with the estimate in Subramanian (2011). The WTO’s mean estimate is that China will account for 17 percent of world trade in 2035, with a range of 11–23 percent.

Figure 2.7 Number of New Signed Preferential Trade Agreements, 1958–2012

Note: The year of the count is the year of notification of the agreement to the WTO. To simplify the classification of agreements, included in the “economic integration agreement” category are all agreements that are both economic integration agreements and customs unions or partial scope agreements.

An interesting new dimension of these PTAs is the extent to which they feature “deep integration” (Lawrence 1996)—that is, liberalize not only tariffs and quotas but other “behind-the-border” barriers, such as regulations and standards, as well. In the last 10 years, for example, nearly 40 agreements have included provisions on WTO–Plus issues (competition policy, intellectual property rights, investment, and the movement of capital). This figure is four to five times greater than comparable agreements in the pre–WTO era (WTO 2011) (see figure 2.7 and table 2.4).

In part because of these deep integration agreements, it would be wrong on the basis of the tariff evidence to underestimate the potential discriminatory effect of preferential arrangements. In agriculture and some manufacturing sectors, such as textiles, tariffs are still high. In services, any future deepening of preferential agreements could create significant discrimination against outsiders, because most favored nation (MFN) levels of protection are significant and there is considerable scope for the preferential recognition of standards, licensing, and qualification requirements. Strong exclusionary effects could also arise from “deeper integration” along other dimensions: preferential agreements increasingly have provisions on investment protection, intellectual property rights, government procurement, competition policy, and technical barriers to trade. A discriminatory tariff may matter less than the selective recognition of product safety standards or selective access to government procurement markets.

Table 2.4 Number and Type of Preferential Trade Agreements

| Type of agreement | Pre–WTO | 1995–2000 | Post-2000 |

|---|---|---|---|

| WTO+ issues | |||

| Customs | 13 | 11 | 56 |

| Antidumping | 12 | 8 | 53 |

| Countervailing measures | 4 | 5 | 52 |

| Export taxes | 8 | 8 | 41 |

| State aid | 10 | 9 | 34 |

| Trade-related intellectual property rights | 6 | 4 | 41 |

| Services | 7 | 2 | 39 |

| State trading enterprises | 5 | 3 | 35 |

| Technical barriers to trade | 2 | 2 | 36 |

| Sanitary and phytosanitary standards | 2 | 1 | 35 |

| Public procurement | 5 | 0 | 32 |

| Trade-related investment measures | 6 | 2 | 31 |

| WTO plus X issues | |||

| Competition policy | 11 | 9 | 19 |

| Movement of capital | 6 | 5 | 38 |

| Intellectual property rights | 5 | 2 | 39 |

| Investment | 4 | 1 | 35 |

Source: Baldwin 2011b.

Note: WTO+ provisions concern commitments that already exist in WTO agreements but go beyond the WTO disciplines. WTOX provisions cover obligations that are outside the current WTO aegis.

On regional agreements, seismic changes are under way, with the possible negotiation of mega-regional agreements between the United States and Asia (the Trans-Pacific Partnership) and the United States and Europe (the Transatlantic Trade and Investment Partnership). Trade between these groups of countries accounts for about $2–$3 trillion a year in world trade, signifying a potentially major jump in the volume of trade covered by preferential agreements. These PTAs would represent the first between the top four major regions of the world (China, the United States, Europe, and Japan), with consequences that will be discussed below. If the Transatlantic Trade and Investment Partnership and Trans-Pacific Partnership (to the extent that it includes Japan) are concluded, more than half of global trade will be covered by those deeper regional agreements. It is not unforeseeable to think of an era in which nearly all trade becomes regional.

Lower Formal Barriers in Goods, High Barriers in Services

The world has become much less protectionist. Globally, MFN tariffs have declined from more than 25 percent in the mid-1980s to about 8 percent today. Border barriers (tariffs and nontariff measures) in manufacturing in the Organisation for Economic Co-operation and Development (OECD) countries are less than 4 percent.

Figure 2.8 Average Most Favored Nation Tariffs by Income Group, 1981–2009

Note: Spikes may reflect entry and exit of countries in the sample.

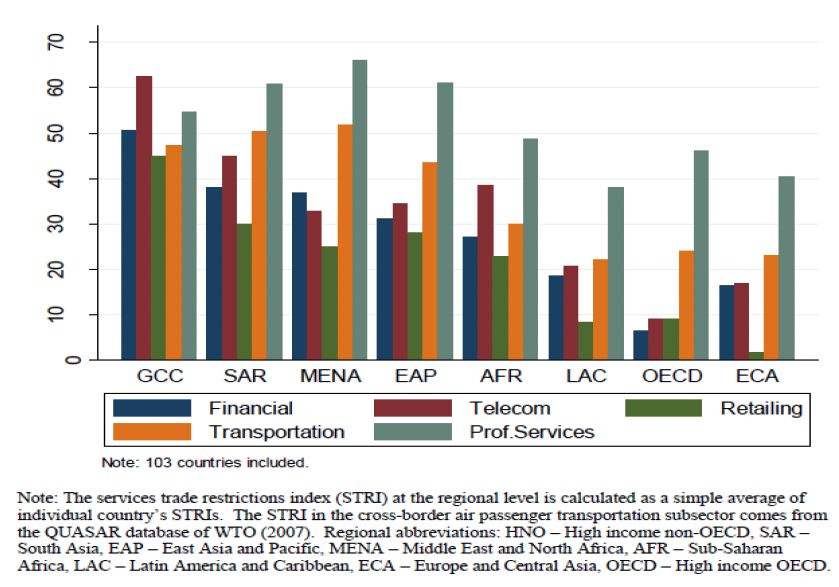

The U.S. International Trade Commission (USITC 2011) estimates that the welfare gains in the United States from eliminating all remaining tariffs are close to zero. Border barriers in the larger emerging markets are higher, but they have declined considerably, from about 45 percent in the early 1980s to just over 10 percent in 2009 (figure 2.8). But barriers to trade in services remain high.14 Borchert, Gootiz, and Mattoo (2012) calculate restrictiveness trade indexes for services. They cover five major sectors—financial services, telecommunications, retail distribution, transport and professional services—and the different modes of delivering these services across borders cross-border and via investment abroad). The index ranges from 0 (completely free) to 100 (completely restricted). Barriers vary across service sectors, but the average level is high (figure 2.9). 15 Barriers are relatively low in telecommunications and relatively high in transportation and professional services. They also vary across regions: Latin America is nearly as open as OECD countries, whereas Asia and the Middle East have high barriers. In fact, as in goods, barriers are correlated with a country’s level of development (figure 2.1). What this means is that international negotiations will increasingly focus on services and FDI.

Figure 2.9 Index of Services Trade Restrictiveness, by Sector and Region, 2008–10

14 There are no data on barriers to trade in services going back in time that would allow a quantitative description of changes in barriers.

15 This index cannot strictly be compared with tariffs, but the farther away the number is from zero, the less open a country is.

Figure 2.10 Index of Services Trade Restrictiveness and per Capita GDP

Two points are worth noting. First, barriers to trade in goods and services have declined sharply over time; the world as a whole is thus becoming less closed. But the composition of world trade is shifting toward the poorer countries (especially toward China and India), and these countries are on average more protectionist (as figures 2.8–2.10 illustrate). The composition of world output is also shifting toward services and away from manufacturing. Both these compositional shifts make the world as a whole less open and attenuate the liberalization trend that stems from all countries reducing barriers.

Second, the integration of goods and services markets is nowhere close to completion. One way of assessing how far from full globalization the world still is might be to compare actual trade with what is predicted by a simple gravity model without frictions. As Krugman (1995) and Anderson (2011) show, under frictionless trade, the world trade share is inversely related to the distribution of GDP across countries: the more equal the distribution, the greater the world trade share. In 1970, actual trade was about 10 percent of the theoretical maximum predicted by the frictionless gravity model. In 2011, it was about 40 percent (perhaps less if trade is calculated on a value-added basis). Thus, although actual trade is rapidly catching up with trade in a frictionless world, there is still some way to go.16

3. Three Pressing Proximate Challenges

This section discusses three recent challenges that have emerged in the trading system and proposes potential solutions to each of them. The proposed solutions can never be reached on their own, however, unless the deeper and more fundamental challenges, discussed in subsequent sections, are addressed.17

Trade and Currency Wars

Mercantilism and self-insurance: The dual origins of reserve accumulation

In the late 1990s, in the aftermath of the Asian financial crisis, a number of emerging market countries, especially in Asia, adopted an economic strategy that was dubbed Bretton Woods II (Dooley, Folkerts-Landau, and Garber 2003). This strategy had two motivations and one manifestation. Reeling from the disruption that sudden withdrawal of foreign capital had caused to their economies and chafing at the political humiliation of having to borrow from the IMF, they decided to self-insure against future crises.18 Self-insurance took the form of building an arsenal of foreign exchange reserves (see the paper by Allen and others on this website; Goldstein 2009). The second motivation was mercantilism, a strategy that made trade surplus the engine of growth.

Both motivations translated into a common manifestation: countries moved from being large net importers of finance (running large current account deficits) to being less reliant on finance, or in some cases, notably China, Malaysia, and Taiwan (China), to becoming net exporters of finance (running current account surpluses). These motivations also translated into—actually require—a policy of undervaluing the exchange rate in a fixed or managed peg regime, aided by intervention in foreign exchange markets. A few countries in East Asia (China and Malaysia in particular) tended to maintain restrictions on capital inflows as a way of sustaining a competitive exchange rate.

16 An implication of this finding on unrealized globalization is that going forward, this potential is likely to be greater in services than in goods.

17 The next section, on trade and currency wars, draws on Mattoo and Subramanian (2009).

18 The perceived humiliation was captured in the picture of the IMF Managing Director at the time, Michel Camdessus, looking over a head-bent President Suharto signing the economic adjustment program with the IMF.

Bergsten and Gagnon (2012, p. 2) argue that more than 20 countries have been intervening in foreign exchange markets for several years “at an average rate of nearly $1 trillion annually… to keep their currencies undervalued and thus boost their international competitiveness and trade surpluses.” These countries include China and a number of East Asian countries, oil exporters, and some advanced countries, including Israel and Switzerland.

This problem is not new. Similar issues of undervaluation arose relating to the Deutsche mark in the 1960s and the yen in the 1970s and 1980s. The mercantilism or currency wars of today are related to the much deeper problem—and some would argue the greatest design flaw in the Bretton Woods system—of the asymmetric adjustment between surplus and deficit countries in the international monetary and trade system. Bergsten and Gagnon (2012, p. 10)) write that “it is a huge irony that the Bretton Woods system was created at the end of the Second World War primarily to avoid repeating the disastrous experiences of the inter-war period with competitive devaluations, which led to currency wars and trade wars that in turn contributed importantly to the Great Depression, but that the system has failed to do so.”

Consequences of mercantilism

Why are current account surpluses combined with undervalued exchange rates a problem for the international economic system? The consequences or problems can be categorized as cyclical mercantilism, structural mercantilism, and macro-mercantilism.

Cyclical mercantilism arises when the economy is depressed relative to trend growth; such a situation is characterized by idle resources, underutilized capital, and unemployment. Mercantilism by one country threatens deflation in partner countries facing idle resources. This concern preoccupied Keynes, who argued that because of international liquidity constraints, there would always be greater pressure on debtors (countries running deficits) to adjust than on creditors. This asymmetry would impart a deflationary bias, because debtor countries would have to cut demand without surplus countries having to undertake the offsetting reflation. He therefore proposed that pressure be exerted on creditor countries by forcing them to pay instead of receiving interest on their positive balances (see Williamson 2010).

In the current context, the deflationary impact of Chinese policies on the United States, quantified by Cline (2010), has prompted some commentators to call for aggressive trade action by the United States against China and other countries practicing mercantilism (Krugman 2010; Bergsten and Gagnon 2012). Persistent surpluses by Germany and their deflationary impact, especially within Europe, have sparked similar calls for action (Wolf 2010).

Structural mercantilism arises when a country pursues policies such as undervalued exchange rates as development or growth policy for an extended period of time. Such policies can have long-run effects on partner countries. An undervalued exchange rate is both an import tax and an export subsidy; it can have adverse effects on trading partners. One way structural mercantilism is transmitted is by depressing the medium-run price of manufactured products, reducing opportunities for specialization in manufacturing and manufactured exports in partner countries. The concerns expressed in Sub-Saharan Africa and Latin America relate to structural mercantilism. Mattoo, Mishra, and Subramanian (2012) show, for example, that a 10 percent depreciation of China’s real exchange rate reduces a developing country’s exports of a typical product to third markets by about 1.5–2.0 percent. Such a decline can have long-run growth effects.

Macro-mercantilism was most evident in the recent crisis in the creation of the so-called savings glut (Bernanke 2005, 2007). Large and growing aggregate current account surpluses increase global liquidity, leading to easy credit and lending, which can easily morph into imprudence, financial excess, and asset bubbles, threatening financial stability. The savings glut hypothesis is by no means uncontested; many economists argue that monetary and regulatory policies in borrowing countries should bear the brunt of responsibility (Johnson and Kwak 2010; Haldane 2010). How much blame the bartender should bear for plying alcohol on a drinker who binges will forever be disputed. But that excess liquidity was a factor and that Chinese mercantilist policies created excess liquidity are plausible deeper causes of the Lehman crisis (see Bernanke and others 2011).

Currency wars or the resulting global imbalances are a systemic problem only if one or a few large countries pursue them. The possibility of collective action to prevent them must take account of this reality.

Exchange rates and foreign exchange intervention are centrally implicated in mercantilism. The international monetary system, under the auspices of the IMF, is therefore the best forum in which to find a solution. The prospects for any serious reform remain slim, however, because of the inherent limits to international monetary cooperation. Systemic threats arise from the policies of the largest countries, in particular when polices pursued in self-interest conflict with the collective interest. But, by definition, it is difficult for the rest of the world to change the incentives of the large country to give more weight to the collective interest. Successful cooperation is fated to falter if not fail—and the efforts of the IMF in this matter have often resulted in failure. As Mussa (2007) makes clear, “In none of these consultations has the Executive Board ever concluded that a member was out of compliance with its obligations regarding its exchange rate policies or any other matter” (emphasis in the original).19

Williamson (2011, p. 1) notes that “it has been 80 years since John Maynard Keynes first proposed a plan that would have disciplined persistent surplus countries. But the Keynes Plan, like the subsequent Volcker Plan in 1972–74, was defeated by the major surplus country of the day (the United States and Germany, respectively), and today China (not to mention Japan or Germany) exhibits no enthusiasm for new revisions of these ideas.” The question is whether there is anything that the rest of the world could have done—by way of sticks or carrots—to have persuaded the United States in 1944, Germany in 1973, or China in 2007 to change its positions or policies for the collective good.

19 Keynes himself recognized the asymmetry of IMF leverage between creditor and debtor countries in the discussion in the lead-up to the creation of the IMF.

The IMF’s ineffectiveness is a proximate manifestation of deeper structural causes related to leverage and legitimacy. Although the IMF has been able to effect changes in member country policies in the context of financial arrangements, it has not been influential without the leverage of financing. In its key surveillance function (which involves no financing), the IMF has rarely led to changes in the policies of large creditor countries, even when such policies have had significant spillover effects on countries; it has not been able to persuade large creditor countries to sacrifice domestic objectives for systemic ones. There seems to be an implicit “pact of mutual nonaggression,” to use Mussa’s phrase, in IMF surveillance. Perhaps as a result, the IMF has had a history and tradition of nonadversarial dialogue between its members and has not had to develop a real dispute settlement system.20

Compounding this problem of limited leverage is the IMF’s eroding legitimacy. Although its role and importance were rehabilitated with the recent global financial crisis, the perception of the IMF as an unreliable interlocutor in emerging market countries—Asia in particular—endures. A good example is the IMF’s new conditionality-lite financing facility, which has few takers because some emerging market countries do not want to be seen as even potential borrowers from the IMF. Indeed, in 2009, a number of emerging market countries—Brazil, Singapore, and the Republic of Korea—preferred to get lines of credit from the U.S. Federal Reserve than the IMF.

The WTO seems to be different on these two counts of legitimacy and leverage, because it works on the basis of the exchange of concessions, which ensures that all players feel that they have derived a fair political “bargain.” Reciprocity ensures political buy-in to cooperation. Periodic negotiations in the GATT/WTO have updated this political contract between countries, redressing some old grievances and papering over others, with the implicit understanding that there will be a future occasion to take up the unsolvable problems of the day.

20 A corollary of the observation that cooperation is least likely where the self-interest of the largest countries are at stake is that the prospects for successful cooperation are greater where these countries are less affected and when the demands on them are minimal. Building global safety nets by providing greater and more expeditious access to crisis financing is one area where the greatest progress has already been made. The IMF’s lending ability tripled after the crisis, and it may increase further. For the large countries, it is both desirable and effective to push for larger safety nets. The costs are relatively small— involving larger financial contributions rather than any major change of domestic policies—and the rewards are great, because the system as a whole is strengthened while the individual clout of the large countries is increased (see Goldstein 2009).

A consequence of reciprocity and the periodic updating of the political contract to cooperate— and another reason why the WTO works—is that this process creates incentives to adhere to the dispute settlement contract. Dispute settlement by the WTO is effective largely because countries feel that they have previously (and recently) made a reasonably advantageous, fair, and equitable bargain, to which they must adhere. WTO governance works because negotiations to create the rules and agree on liberalization are perceived as fair and broadly equitable in outcome, rendering subsequent compliance possible.21

Trade, Climate Change, and Green Growth

Do the institutions and ideology of globalization come in the way of tackling climate change? In one very important respect, they may.22

Consider two episodes from 2012. In late 2012, the United States and the European Union sanctioned the use of antidumping duties against Chinese exports of solar panels on the grounds that Chinese manufacturers were “dumping” (selling below cost) solar panels manufactured in China. In the presidential debates, President Obama was on the defensive against Mitt Romney, who tried (with some success) to tar him with the “failed industrial policy” brush in relation to government support for clean energy and Solyndra, a producer of solar panels that filed for bankruptcy two years after receiving substantial government loans and guarantees. These examples illustrate how international rules and ideology (which underlie rules) could come in the way of efforts to tackle climate change.

Mattoo and Subramanian (2012b) argue that only radical technological change can reconcile climate change goals with the development and energy aspirations of the bulk of humanity. Technological change requires the deployment of the full range of policy instruments that would raise the price of carbon and provide incentives for research and development of noncarbon-intensive sources of energy and related green technologies. With notable exceptions, countries have shown great reluctance to raise the price of carbon directly.

21 Experience suggests that the mere prospect of retaliation, as well as the reluctance to be seen as a rule breaker, is sufficient to ensure compliance and that there is rarely need for action.

22 This section is based on Mattoo and Subramanian (2013).

International rules severely restrict the use of subsidies. Under current WTO rules, domestic subsidies for the development and production of clean energy and related energy technologies are actionable by partner countries if those countries feel that their domestic production or exports are adversely affected. Until 2000, some of these subsidies were deemed nonactionable, but the exemption has not been renewed. Moreover, all forms of export subsidy involving clean energy and/or green technologies are prohibited. These rules are in place because of the ideology that imbues globalization—the notion that subsidies and all forms of industrial policy are dubious.

In relation to climate change, these rules are doubly bad. There is, of course, a logic to curtailing subsidies: even if they confer domestic benefits, those benefits are outweighed by the damage to partner countries. A multilateral rule to which there is general adherence reduces that damage, potentially leaving countries better off. But in the case of climate change, because spillovers are global, any subsidy that promotes clean energy and development confers a benefit to partner countries. On balance, therefore, rules should err on the side of promoting rather than restricting subsidies.

There is a second, arguably bigger, political economy benefit. Prospects for climate change action in the United States in the form of a carbon tax or cap-and-trade are not bright. President Obama’s grand rhetoric in his 2013 State of the Union speech is unlikely to be matched by bold action because of the lack of bipartisan support in Congress. This state of affairs reflects a combination of factors—climate change denial, the strength of the carbon energy industries, and weak economic prospects. There is probably only one development that could galvanize action in the United States: the threat that China will capture green technology leadership. The United States needs a Sputnik moment of collective alarm at the loss of economic and technological ascendancy.

The problem is that China is currently constrained by WTO rules, as the actions against its firms in 2012 illustrate.23 China and all countries that are not straitjacketed by the tyranny of the susbsidies-are-bad ideology and that have the financial means to do so should be allowed to deploy industrial policy to promote clean energy and green technologies. If doing so leads to a subsidy war because partners feel threatened, that is a war that should be promoted, as it will ignite the race for the development and production of an undersupplied global public good. From this perspective, WTO rules should allow not only domestic but also export subsidies; current rules circumscribe the use of domestic and prohibit the use of export subsidies.24

Trade and Scarcity of Food and Resources

The 2007 global food crisis was severe.25 According to the World Bank, about 100 million people are estimated to have been thrown back into the ranks of the poor because of increases in the price of food. Riots occurred in a number of countries. The Bank identified 33 countries as especially vulnerable. The poor were especially vulnerable because they spend the largest portions of their income on food. In the United States, the poor spend an estimated 18 percent of their income on food; a similar measure for households earning less than $1 a day is about 72 percent in Peru and South Africa, 66 percent in Indonesia, and 50 percent in Mexico (Banerjee and Duflo 2011).

23 In fact, China stopped providing subsidies to its solar power companies in response to trade action by the United States. “The U.S. Trade Representative’s Office responded by filing a complaint in December with the WTO saying China violated rules of the Geneva-based trade arbiter. China’s Special Fund for Wind Power Manufacturing required recipients of aid to use Chinese- made parts and amounted to a prohibited subsidy, the U.S. said. Before the WTO acted on the complaint, China made it moot by ending that aid in June, according to the U.S.” (http://www.bloomberg.com/news/2011-09-23/blame-china-chorus-grows-as-solyndra-fails-amid-cheap-imports.html).

24 Another area in which trade restrictions should be permitted are border tariffs against imports from countries that do not tax carbon in the manner that the importing country does. Such tariffs would help overcome opposition from energy-intensive industries in countries wishing to raise the price of carbon on the grounds that they would be rendered uncompetitive relative to imports from countries that do not tax carbon. A final area in which WTO rules need to be clarified is export restrictions on natural gas, which is becoming an important fuel. The U.S. currently limits its exports to countries with which it does not have a free trade agreement. If greater global use of natural gas is desirable (because it is cleaner than substitutes such as oil and coal), then restrictions on exports may be deleterious for global energy emissions.

25 This section draws on Mattoo and Subramanian (2012a).

But pressure on food supplies, and associated high food prices, could be a medium- to long-term reality, because some of the driving factors—rising prosperity in the developing world, which creates more demand; high fuel prices; stagnant agricultural productivity; and climate change– induced pressure on agricultural supplies, including through the depletion of water—could be of a durable nature. These fundamentals are being exacerbated by export restrictions on foodstuffs. According to a World Bank report, in the 2007 crisis, 18 developing countries imposed some form of export restrictions (Zaman and others 2008). Each country was trying to keep domestic supplies high, on the grounds of food security. But as more countries implemented export controls, global supply contracted, pushing prices up and exacerbating global food insecurity. The global rice market was particularly affected by trade restrictions.26

There are few restrictions on the use of export taxes in the WTO, and its disciplines on export restrictions are incomplete. The GATT does prohibit quantitative restrictions on exports, but temporary restrictions are permitted in order to prevent critical shortages of food or other goods.

This permissiveness on export taxes and restrictions is resulting in the worst of all possible worlds. Under “normal” agricultural conditions, costly taxpayer support reduces imports and encourages production and exports, creating huge distortions. Under abnormal conditions, such as are prevailing now, the opposite occurs: countries liberalize their imports but prevent exports. What is needed is a system in which both imports and exports remain free to flow in good times and bad. Such a system is especially important if trade is to remain a reliable avenue for food security. If in bad times importing countries are subject to the export-restricting actions of producing countries, they will consider trade an unreliable way of maintaining food security and reconsider how to manage their agriculture. As a result, there will be a greater temptation to move toward more self-reliance as insurance against the bad times.27

26 Food security goals are best served not by restricting trade but by deploying domestic policy instruments such as targeted safety nets. The existence of such safety nets would dilute the political economy bias in favor of trade interventions.

27 Not surprisingly, WTO members that depend heavily on world markets for food (for example, Japan and Switzerland in 2000; the Democratic Republic of Congo, Jordan, and the Republic of Korea in 2001) have pushed for disciplines on export controls and taxes. Recognizing that importers’ concerns about the reliability of supply could inhibit liberalization, some exporting countries have advocated for multilateral restrictions on the right to use export restrictions (examples include the Cairns Group and the United States in 2000 and Japan and Switzerland in 2008) (International Economic Law and Policy Blog 2008).

The Doha Round of trade negotiations did not address these problems. It was devoted to traditional forms of agricultural protection—trade barriers in the importing countries and subsidies to food production in producing countries—which are now becoming less important as food prices have soared and import barriers declined. The trade agenda needs to be enlarged, so that trade barriers, on both imports and exports, are put on the trade agenda.

Trade policies have also exacerbated the scarcity of nonfood resources. Concerns have already arisen over China’s restriction of exports of rare earth metals, for some of which (for example, scandium and yttrium) it accounts for more than 70 percent of the world’s exports. It also accounts for a large shares of exports of other key raw materials, including various forms of bauxite, magnesium, and zinc.28

4. Fundamental Policy Challenges

The period of hyperglobalization has been associated with the most dramatic turnaround in the economic fortunes of developing countries. Regardless of the view one takes about this association, it is safe to say that a broadly open system is good for the world, good for individual countries, and good for average citizens in these countries. Going forward, even if the pace of hyperglobalization slows, the aim of policy at the national and collective level must be to sustain steady and rising globalization and avoid sharp reversals.

The previous section illustrated some of the proximate challenges. They can be addressed only if the deeper challenges are recognized and addressed.

One way of approaching these more fundamental policy challenges is suggested in table 4.1, which helps identify the problems and hence to prioritize the policy response. This schematic can be applied to three broad groups of countries (high, middle, and low income), the challenges and responses for each of which may differ.

28 In an earlier case, a WTO panel ruled against certain export restrictions China had maintained on a number of raw materials, including bauxite, coke, fluorspar, magnesium, and zinc.

Table 4.1 Policy Responses to the Challenges to Globalization

| Level of response | Further liberalize | Maintain status quo | Retreat from globalization |

|---|---|---|---|

| National | – In low-income countries, strengthen domestic supply capacity to exploit globalization. – In China and other middle-income countries, sustain growth to enable further liberalization. – In high-income countries, revive growth and address “beleaguered middle class” and entitlements problems | Strengthen social insurance in high-income countries. | |

| International/collective | – Prevent fragmentation and conflict. – Sustain multilateralism through a “China Round.” | Cooperate on taxation of mobile factors to sustain domestic safety net. | Create minimum safeguards to allow some trade protection? |

What are the really important challenges for the open trading system, and how should they be responded to? If the next couple of decades mimic or come close to mimicking the last two in terms of globalization, success will have been unambiguous. The challenge is thus simply to maintain the status quo and allow the forces that have shaped globalization over the last few decades to play themselves out.

Alternatively, one could argue that globalization needs to advance on a number of different dimensions—because, for example, impediments remain to the prospects of average citizens, especially in low-income countries. The need for further globalization could also stem from the perception that in some respects, the current system is unsustainable, because it is differentially open and the burden of providing open markets is not equally shared, especially by China.

A third logical possibility is that the forces that will push against globalization are, or will become, so strong that a retreat from current globalization is inevitable. The challenge then will be to manage this retreat in a way that minimizes the costs to countries and citizens around the world.

The responses to each of these challenges can occur at the national level, at the international level, or through some combination of national and collective action. The responses to these challenges are discussed below.

The West’s Challenge: Hyperglobalization Meets Economic Decline

The bad news

Public support for free trade agreements in the United States is at its lowest point since 2006, according to the Pew Center (2010)—and the decline occurred quickly. In 2009, the share of people who supported free trade agreements exceeded the share who opposed it by a margin of 11 percentage points. In 2010, opponents of free trade outnumbered supporters by 8 percentage points. Surprisingly, among Republican-leaning voters, the turnaround was even more dramatic: the margin in 2009 was 7 percentage points in favor of free trade agreements; the margin in 2010 was 26 percentage points against free trade agreements. This weakening collective perception of the benefits of openness is matched, mirrored, or validated by intellectual opinion.

Samuelson (2004) argues that the rise of developing countries such as China and India could compromise living standards in the United States, because as they move up the technology ladder, they provide competition for U.S. exports, reducing their price. Krugman (2008) focuses on the impact of imports from developing countries, particularly China, on the distribution of income in the United States and the wages of less-skilled workers. His conclusion is that “it is likely that the rapid growth of trade since the early 1990s has had significant distributional effects” and that “it is probably true that this increase (in manufactured imports from developing countries)… has been a force for greater inequality in the United States and other developed countries” (Krugman 2008, 134–35).

Blinder (2009) draws attention to the employment and wage consequences of the outsourcing that has been facilitated by technological change and trade in services. He estimates that 22–29 percent of all U.S. jobs will be offshored or offshorable within the next decade or two.

Summers (2008a, 2008b) has highlighted the problems stemming from increasing capital mobility. Hypermobile U.S. capital creates a double whammy for American workers. First, as companies flee in search of cheaper labor abroad, American workers become less productive (because they have less capital to work with) and hence receive lower wages; the “exit” option for capital also reduces the incentive to invest in domestic labor. Second, capital mobility impairs the ability of domestic policy to respond to labor’s problem through redistribution because of an erosion in the tax base as countries compete to attract capital by reducing their tax rates.

Spence and Hlatshwayo (2011) argue that almost all the increase in employment of 27.3 million jobs in the United States between 1990 and 2008 was in the nontradable sectors, where productivity growth was much slower than in the manufacturing and tradable sectors, explaining the long-term stagnation of wages in the last segment of the workforce.

That a constellation of intellectuals—instinctively cosmopolitan and ideologically liberal—talks like this is an important signal, not least because the objective circumstances have changed. One might call this challenge that of the irresistible force of globalization and hyperglobalization meeting the immovable object of weakening economic and fiscal fortunes in the West.

In the United States, except for a brief spell in the late 1990s, median wages have stagnated for three decades; inequality has been sharply rising, particularly because of rising incomes at the very top of the income spectrum (Piketty and Saez 2003); and mobility has declined (Haskins, Isaac, and Sawhill 2008) Worse, as in all industrial countries, indebtedness has risen (average debt in the G-7 is now about 80 percent of GDP), prospects for medium-term growth in the future are not bright (according to the latest World Economic Outlook forecast), and aging and entitlements add to the serious fiscal pressures looming ahead. These objective conditions are not the most propitious for sustaining globalization.

This structural malaise is captured in the following metaphor that Larry Katz, of Harvard, uses: “Think of the American economy as a large apartment block. A century ago—even 30 years ago—it was the object of envy. But in the last generation its character changed. The penthouses at the top keep getting larger and larger. The apartments in the middle are feeling more and more squeezed, and the basement has flooded. To round it off, the elevator is no longer working. That broken elevator is what gets people down the most” (quoted by Luce 2010).

The policy challenge in the advanced countries is that sustaining current levels of openness will require addressing these domestic challenges at the very time when growth could be slowing and the ability to effect redistribution is being impeded by broader medium-term fiscal concerns. In this light, the changing attitudes to globalization and free trade cited above are not surprising.

We focus here on what is now different in the West’s ability to sustain globalization. A starting point is the view, described in Rodrik (1998), that sustaining openness requires a domestic social consensus in its favor, which in turn requires mechanisms of social insurance to cushion domestic actors against globalization-induced shocks. Rodrik (1998) provides evidence showing that this domestic consensus can be captured in the relationship between the size of government (a proxy for social insurance mechanisms) and openness.

More direct evidence of the importance of social insurance comes from a paper by Autor, Dorn, and Hanson (2013), who show that rising exposure to Chinese imports increases unemployment, lowers labor force participation, and reduces wages in local labor markets. They estimate that the exogenous component of this shock explains one-quarter of the contemporaneous aggregate decline in U.S. manufacturing employment. They estimate that rising exposure to Chinese import competition explains about 16 percent of the decline in U.S. manufacturing employment between 1991 and 2000 and 27 percent of the decline between 2000 and 2007. Transfer payments for unemployment, disability, retirement, and health care also rise sharply in exposed labor markets. They estimate the increase in annual per capita transfers attributable to rising Chinese import competition at $32 in the first 10 years and $51 in the last 7 years of the sample, which translates into total expenditure of about $5 billion in the 1990s and almost $15 billion in the 2000s. The deadweight loss of financing these transfers is one-third to two-thirds as large as U.S. gains from trade with China.

Can the West sustain these social insurance mechanisms? According to Summers (2008a), globalization both increases the need for social insurance and undermines the government’s ability to provide it, because it renders more factors, especially capital and high-skilled labor, more mobile and less easy to tax.

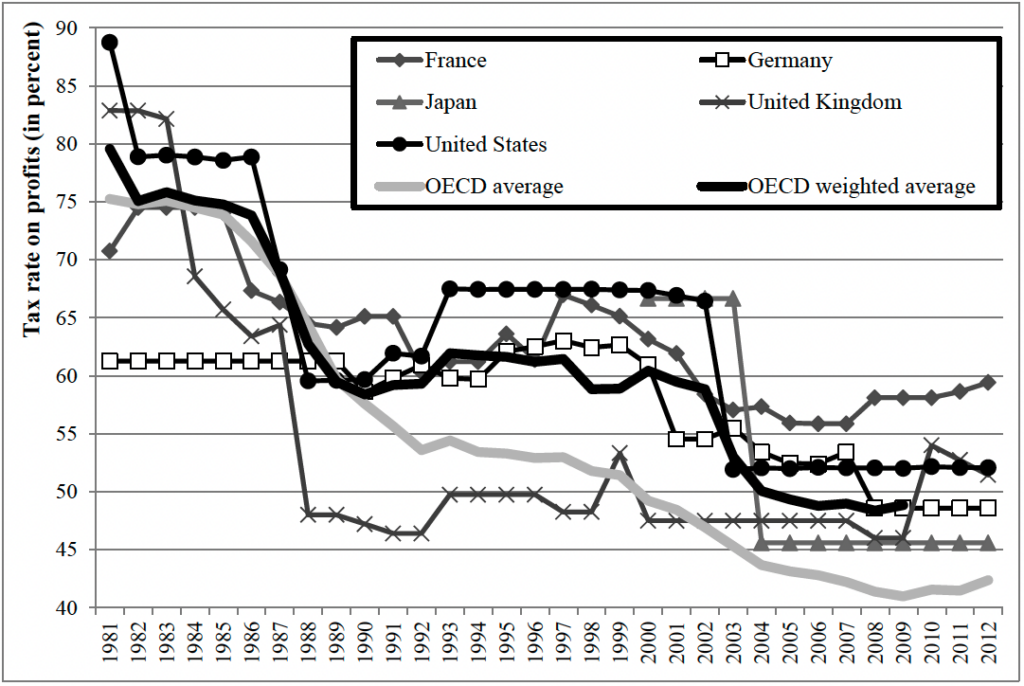

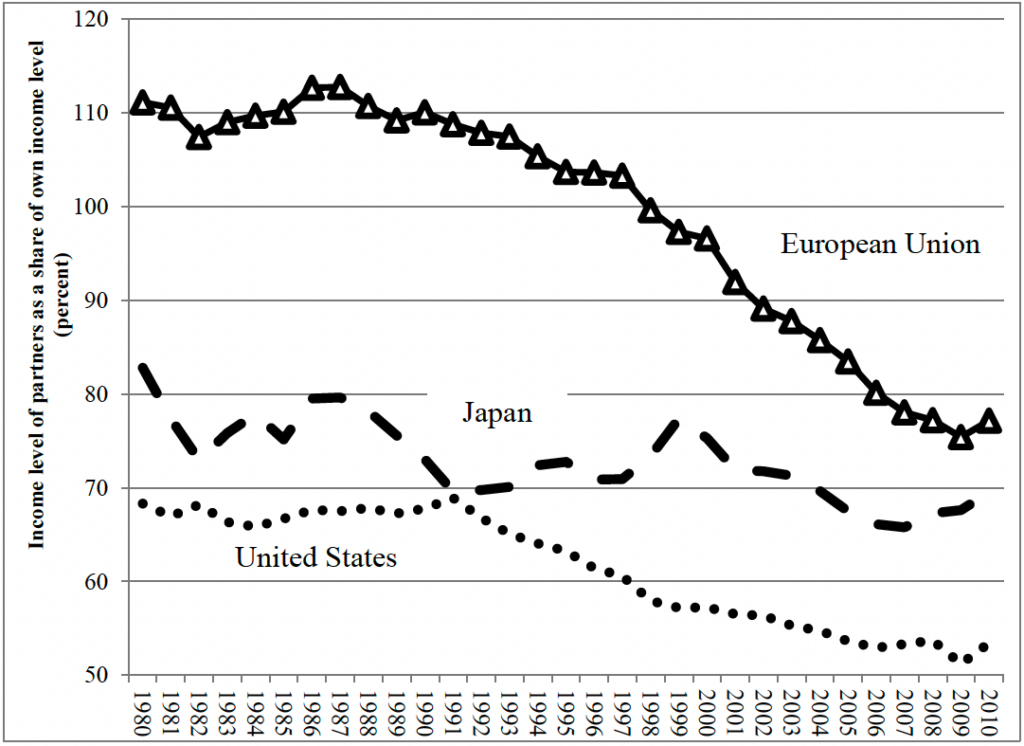

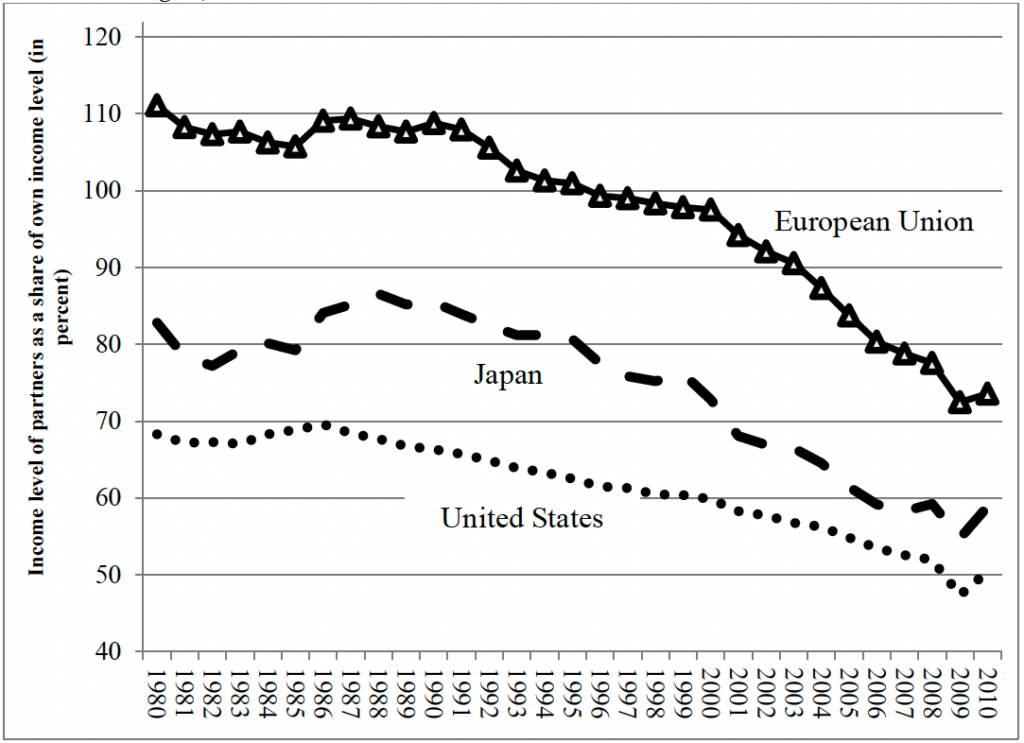

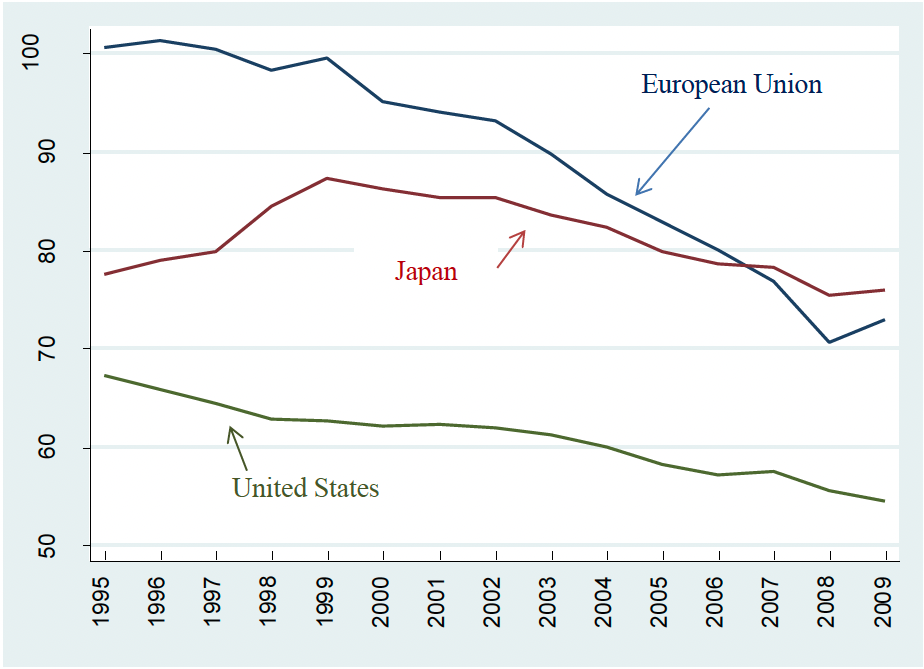

Has capital become less easy to tax? Figure 4.1 plots the marginal effective tax rates on capital in some important OECD countries and for the OECD as a whole. These rates have been sharply declining, and there is little pressure to reverse these trends.

Figure 4.1 Tax Rates on Distributed Corporate Profits in Selected OECD Countries, 1981–2012

Note: Overall (corporate plus personal) tax rate on distributed profits are computed as effective statutory tax rates on distributions of domestic source income to a resident individual shareholder, taking account corporate income tax, personal income tax, and any type of integration or relief to reduce the effects of double taxation.

For the OECD as a whole, the average marginal tax rate declined from about 55 percent to almost 40 percent, a 15 percentage point decline. These declines were witnessed across most if not all countries. In the United States, rates declined from 65 percent to just over 50 percent; in Germany they fell from about 60 percent to less than 50 percent. Of course, these declines reflect pressures other than globalization and the attendant difficulty of heavily taxing mobile capital, but these pressures have been important.

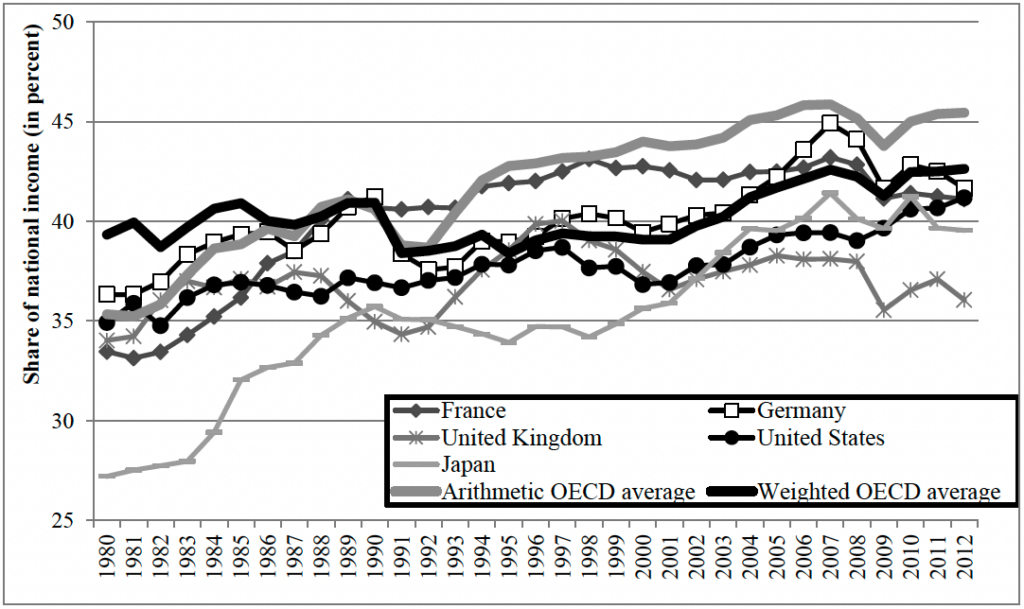

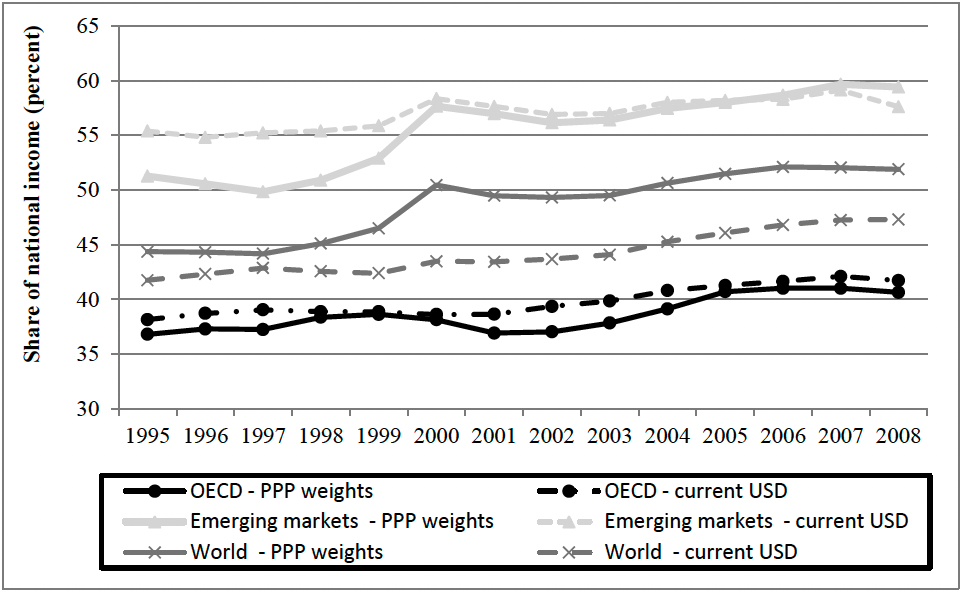

A new development adds to the problems. Across the OECD, the share of the economic pie accruing to capital has been increasing, increasing from about 35 percent to 40 percent in the last few years (figure 4.2). This increasing share has prompted several commentators, including Krugman, to argue that the debate about inequality and trade and inequality in the 1990s, which related to inequality within types of labor (skilled versus unskilled), should now be viewed through a different lens, because inequality is increasingly between capital (and those who own it) and labor.

Figure 4.2 Share of Capital in National Income in Selected OECD Countries, 1980–2012

Note: The share of capital is computed from the AMECO database using the adjusted wage share at current market prices.

For the purposes of our argument, what is important is this: Not only is the ability to finance mechanisms of social insurance being undermined by weak growth and the burden of debt (Ruggie 1998); slippery, mobile capital is now accounting for a larger share of the economic pie. The funding of social insurance through taxation is thus going to become more difficult.

The good news: The protectionist dog that barked but did not bite

Several commentators have remarked on the fact that despite suffering perhaps the biggest global trade shock in the recent global financial crisis, the world did not succumb to protectionism. This response stood in stark contrast to the experience of the 1930s. Explanations for the difference have included the facts that (a) countries could use macroeconomic policy instruments (monetary and exchange rate), which adherence to the gold standard initially prevented in the 1930s (Eichengreen and Irwin 2009); (b) automatic stabilizers were in place, by way of transfers and unemployment benefits (Autor, Dorn, and Hanson 2013); and (c) the deeper integration created by modern production chains rendered protectionism self-defeating (Baldwin and Evenett 2009).

The bigger puzzle is this: How did the West, and the United States in particular, adjust to arguably the biggest structural trade shock in its history—namely, rising imports from China—without any serious recourse to protectionism? Why was there less protectionist outrage in the United States against China than there was against Mexico in the 1990s or Japan in the 1980s? The domestic uproar against China did not match the backlash created in the context of the North American Free Trade Agreement (NAFTA), and actual protectionist actions did not come remotely close to the actions taken against Japan (the Reagan era witnessed the greatest upsurge in trade barriers in the postwar period; see Destler 1992).

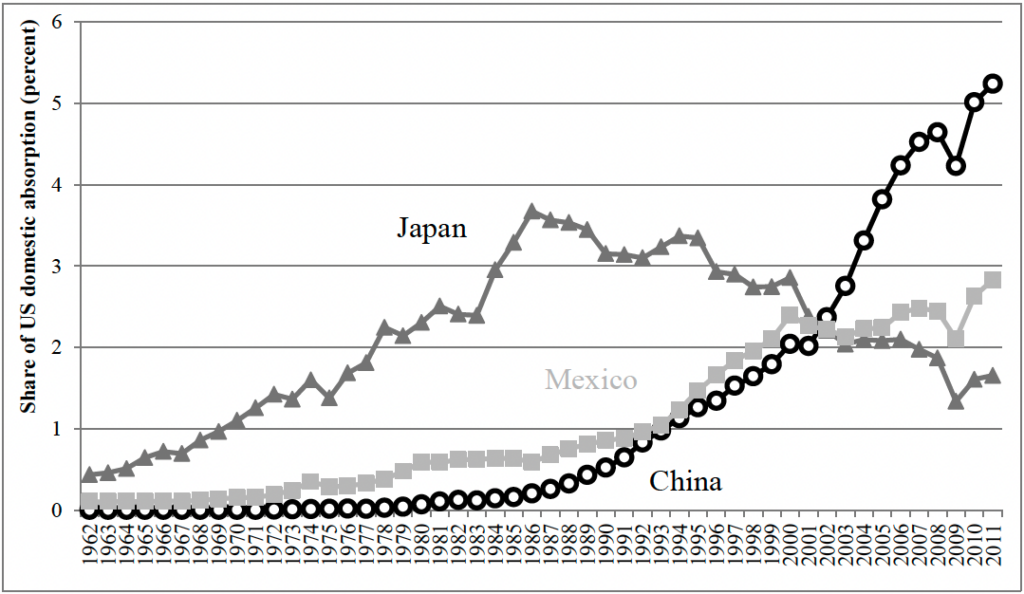

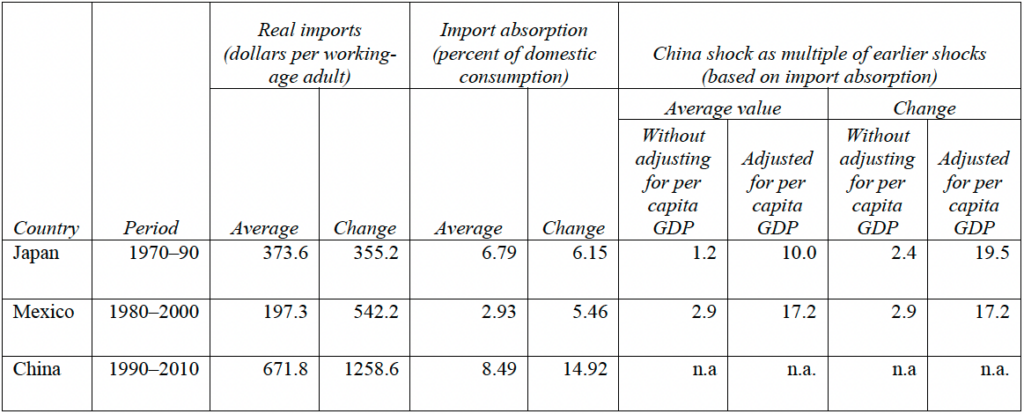

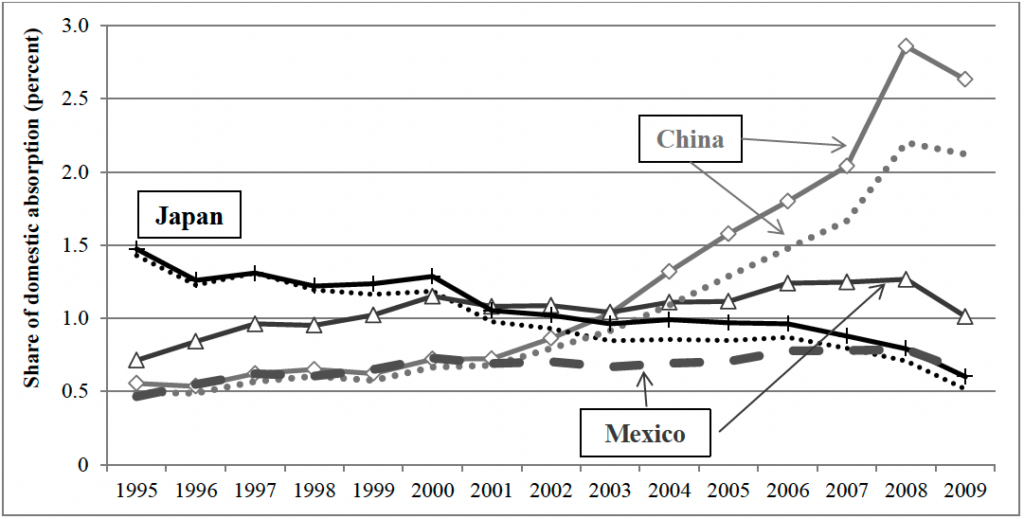

The differences cannot be explained by the relative magnitude of the three shocks, as the Chinese shock was orders of magnitude larger than the early shocks. Figure 4.3 plots imports from Mexico, Japan, and China as a share of U.S. domestic consumption between 1962 and 2011. At their peaks, Japan accounted for 3.6 percent of U.S. consumption, whereas China accounts for about 5.2 percent.29

Figure 4.3 Import Shocks in the United States from Mexico, Japan, and China, 1962–2011

Note: Domestic absorption is GDP minus trade balance.

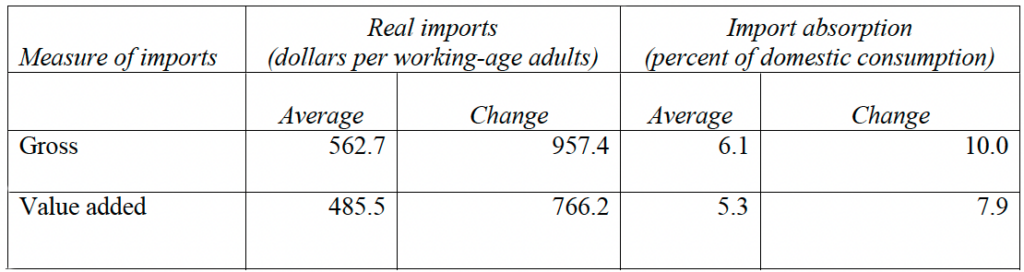

Table 4.2 quantifies the trade shocks to the United States from the three countries. The shock is computed in three ways (each scaled by the working-age population in the United States or the domestic consumption of manufacturing): (a) average imports over the relevant period (for convenience, all shocks are considered to extend over a 20-year period: Japan 1970–90, Mexico 1980–2000, and China 1990–2010); (b) the change in imports over the period30; and (c) both average changes and changes calibrated by per capita GDP in each country.

29 Appendix figure A.3 plots the same data but for a shorter period for which value-added trade data can be computed. Gross exports overstate value-added exports for China, but they overstate them even more for Mexico.

30 Trefler (1993) shows that cross-industry differences in protection are associated with the change in import penetration, not its absolute value. Autor, Dorn, and Hanson (2013) use import penetration as a share of working-age population as the measure of trade shock.

Table 4.2 Magnitude of Import Shocks to the United States from Japan, Mexico, and China